A couple of people have asked what I think about this paper on Chinese infrastructure that is making the rounds, which claims that China “is headed for an infrastructure-led national financial and economic crisis.” It’s rather an obnoxious paper to read, in that it aggressively attacks a straw-man position that few people actually hold, and makes grand macro claims about China based on rather equivocal micro data. The general conclusion is certainly not wrong, though it is a fairly widely held view: China is very likely over-investing in infrastructure, and this is going to have negative consequences for its future growth and debt dynamics. But the actual content of the paper does not do as much to support this view as the authors claim. Here I will try to explain what I think is wrong with the paper, and outline the real reasons why China’s infrastructure investment is problematic.

The core of the paper is an examination of the performance of individual infrastructure projects in China, which the authors compare to projects undertaken in other countries. (The paper’s dataset is exclusively composed of infrastructure projects in China funded by the Asian Development Bank and the World Bank. One might therefore wonder whether the findings say more about the procedures of these multilateral institutions than about China’s unique circumstances. But let’s not quibble.) They find that infrastructure projects in China often cost more and take longer to complete than expected, and that planners often do not accurately forecast demand for the completed projects. Yet these seem to be general problems of large construction and engineering projects around the world:

Actual costs were on average 30.6 per cent higher than estimated costs, with a median of 18.5 per cent indicating that the distribution of costs had a heavy skew to the right (i.e. going over budget). … We found no significant differences in cost overruns between China and rich democracies—i.e. on our sample China’s cost performance is no better or worse than that of rich democracies. …

Similarly, in terms of schedule overrun China performed better than rich democracies. The average schedule overrun in rich democracies was +42.7 per cent (median = +23.0 per cent) compared to Chinese projects’ average of +5.9 per cent (median = 0.0 per cent). Only one in every two projects encountered a schedule delay in China compared to seven out of 10 in rich democracies. …

In the reports we studied for China, the typical BCR [benefit-cost ratio] for transport projects was 1.4 to 1.5, which is broadly in line with many other physical infrastructure assets such as large dams, road, rail, bridge, or tunnel capital investments. In other words, planners expected the net present benefits to exceed the net present costs by about 40–50 per cent.

The authors’ data on individual infrastructure projects tell us that China is basically no worse and no better than the rest of the world in terms of managing infrastructure projects–just like everywhere else, they often run behind schedule and over budget. This is certainly useful information but does not seem like a shocking finding. But if China is no better and no worse than the rest of the world at planning and executing infrastructure projects, it is hard to see how this would lead it into an infrastructure-driven financial crisis. The problem must therefore surely be that China is spending far too much on infrastructure, so that the ordinary problems of project mismanagement are magnified by the scale of its spending.

At this point in the paper I naturally expected the authors to show that China was in fact spending much, much more than other countries on infrastructure. But they don’t. In fact they present absolutely no statistical information about the level or growth rate of infrastructure spending in China. I know, I couldn’t really believe it either. What they do instead is present the usual numbers about the rapid growth of total investment and debt in China, such as the figures on gross fixed capital formation in the national accounts. It should hardly need pointing out that gross fixed capital formation is not the same thing as infrastructure spending; infrastructure is only one component of gross fixed capital formation, most of which is housing and business capital expenditure. (Putting a hard number on China’s infrastructure spending is indeed tricky, but not impossible. According to estimates by the former OECD economist Richard Herd, government and infrastructure sectors have usually accounted for 20-30% of gross fixed capital formation over the past couple of decades.) Since the authors do not establish that China is spending a lot on infrastructure in the aggregate, the conclusion that China’s macro problems from infrastructure spending are much greater than other countries simply does not follow from the micro evidence they present. It would certainly be useful to compare rates of infrastructure investment across countries, but this paper does not do that.

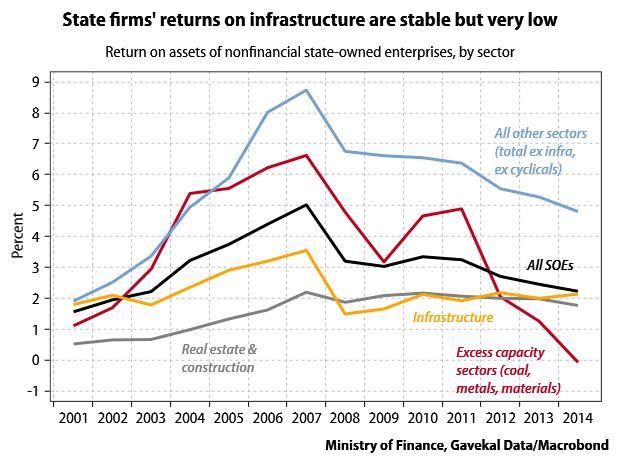

So does that mean infrastructure spending is not an issue for China? Not at all, the issue is very much a real one. I would express it much more simply however: Chinese infrastructure projects generate low financial returns, but have to repay debts at interest rates that are far too high. Here are two numbers to illustrate the point: the average return on assets of state-owned enterprises in infrastructure sectors is around 2%, but the average interest rate that state-owned enterprises pay on their debt is around 5%. It is pretty clear this is not a financially sustainable situation–and note that this is true regardless of what you may think about the broader economic benefits of infrastructure projects, since what matters is the financial returns realized by the project sponsors. And the magnitude is sizable: 6-7 trillion yuan a year, based on Herd’s figures.

It’s an important peculiarity of the Chinese system that so much of its infrastructure is provided by state-owned enterprises, rather than directly by the government. The reasons for this are not totally clear–maybe it helps expedite stimulus spending, or keeps measured government debt low. But the consequences are pretty clear: by channeling a lot of essentially public-sector borrowing through financing channels normally used by private companies, China has created a large financial problem. Since the returns on infrastructure projects are on average not high enough to repay the debt SOEs take out to fund them, if the government does not want the projects to default then it needs to restructure the debt into lower-cost government obligations. This is exactly what is happening now. And since infrastructure investment is still growing by around 20% annually, and returns on infrastructure investment could plausibly fall even further (capacity utilization at thermal power plants is already at a 20-year low due to excess capacity), China will be dealing with this infrastructure debt problem for a while.

Quote from the document: “Only if infrastructure investment ‘grows by 15 to 18 percent (per year), can we reach 8 percent economic growth’ said *Mr Zeng Peiyan*, the former minister in charge of China’s State Development Planning Commission 1 (The New York Times, 24 September 1998). At the time, Asia was in the midst of a financial crisis. Redoubling investment in infrastructure was China’s strategy to slip past the regional downturn. *Mr Peiyan’s* view finds emphatic support in the extant literature in economics and with policy experts.”

If the authors can’t even get basic Chinese naming conventions right, then they are disconnected to a degree that disqualifies the entire document.