(This post reproduces a thread I wrote on Twitter/X on July 29.)

A lot of the discussion about the depreciation of/undervaluation of China’s real effective exchange rate takes for granted that this is about the currency. After all, it’s called the “exchange rate”!

But it’s actually not. Mostly, it’s about prices. A rant:

China’s real effective exchange rate (REER) is a composite of two things, each themselves a composite: 1) an index of the renminbi’s exchange rate against a group of its trading partners, weighted by trade, 2) an index of China’s prices relative to its trading partners.

The standard reference for the REER is the calculation by the BIS. Its numbers show the pure currency part, the nominal effective exchange rate, is now right back at the recent peak of March 2022. The CFETS index, the trade-weighted exchange rate targeted by the PBOC, is not too different.

The REER, however, is down 14% from its peak in 2022. And that is purely, 100%, because of relative prices. Almost all of the move came in 2022-23, when China had a massive deflationary episode while the rest of the world had continued inflation.

So when people say, China’s real effective exchange rate has depreciated or is undervalued, the thing in the real world they are referring to is that prices in China (the CPI for this calculation) have stayed basically flat while rising elsewhere in the world.

Why has this happened? Ultimately, the domestic price level in an economy is under the control of the monetary authorities. This means that it is China’s own choice (mostly through inaction) to tolerate this persistent deflation/disinflation.

Many of China’s trading partners are understandably unhappy with this situation. China’s macroeconomic choices have had the effect of supercharging its export competitiveness: everything in China substantially cheaper relative to the rest of the world.

But there is debate over how to get the desired appreciation of the REER. Some people say that this issue could be solved if you could force China to simply revalue its nominal exchange rate, i.e. raise it enough to get rid of that 14% gap.

The problem with this idea is that a) you can’t force China to do something it doesn’t want to do, b) it’s not clear that a change in the nominal exchange rate would, in isolation, actually work to push up the domestic price level.

My view is that an appreciation of China’s REER is very much to be desired, but the real (haha) way to get there is through higher inflation domestically, and that means different macro policies.

Plus, if the markets recognized that China was actually doing more inflationary macro policy, the nominal exchange rate would appreciate, so you would get a double whammy of a rising price level and a rising exchange rate that would wipe out the REER depreciation.

The ultimate question, which no one has the answer to, is how to convince the Chinese authorities that different macro policies are required. I think complaining about trade surpluses and excess capacity has not worked, and is not going to work.

The key issue, in my view, is the domestic labor market, the true casualty of this tolerance of deflation. Policy decisions have condemned a generation of Chinese youth to widespread under- and un-employment. This is a political pressure point that might actually produce change.

If China would just pursue a conventional macro policy of moderate inflation and full employment, its own citizens would benefit massively and its trading partners would be much happier. There would be peace on earth and goodwill toward men! 🙂

Another good year for music. Thanks to some lucky coincidences I saw the Sun Ra Arkestra, led by Knoell Scott, three times this year. Every show was different, and each a fun and life-affirming musical experience—see them if you can! Their most recent studio album is very charming, even if it lacks the wild avant-garde energy of yesteryear. The best-known standard-bearers of today’s jazz avant-garde, guitarist Mary Halvorson and saxophonist James Brandon Lewis, both had outstanding albums this year (About Ghosts and Abstraction Is Deliverance) that have been widely reviewed; if you follow jazz you probably know about them already. I liked both records a lot, but for my list this year I wanted to highlight some other names. Here are my favorite discoveries from a year of listening, listed by date of original release:

Vijay Iyer & Wadada Leo Smith – Defiant Life (2025). At 84, Smith remains astonishingly productive, a true jazz elder at the height of his powers. His second collaboration with pianist Iyer is if anything even more wrenchingly beautiful than the first, A Cosmic Rhythm With Each Stroke from 2016; they should record more than once a decade. Smith’s abstract yet lyrical trumpet playing also appeared this year on another duet album, Angel Falls with Sylvie Courvoisier—also worth hearing but for me not quite at the same level—and two records with Danish guitarist Jakob Bro that I haven’t heard yet but look promising.

Nels Cline – Consentrik Quartet (2025). One of the best small-group jazz albums of the year, out of a strong field. Cline’s quartet, featuring his guitar with the twisty tenor of Ingrid Laubrock, Chris Lightcap on bass and Tom Rainey on drums, feels like a real band with its punchy rhythmic drive. But the group isn’t locked into one style, and the varied tunes cover a lot of compositional ground.

Cosmic Ear – Traces (2025). Christer Bothén was one of Don Cherry’s collaborators during his Scandinavian sojourn in the 1970s, and for this recording he gathers some fellow travelers for a heartfelt homage to Cherry’s style of spiritually inflected world jazz. It’s as good or better as anything from that era. Bothén’s bass clarinet is also featured on Jorden vi ärvde by the Vilhelm Bromander Unfolding Orchestra, a marvelous large-ensemble recording.

Webber/Morris Big Band – Unseparate (2025). The two co-leaders use the resources of the jazz big band in nontraditional ways, finding all kinds of new combinations of sounds. Continuously inventive and surprising; a sterling example of what people are calling the “New Brooklyn Complexity.”

Marty Ehrlich – This Time (2025). The horn-bass-drums trio is perhaps the most fundamental type of jazz group, and I find increasingly gravitate toward the directness of this format. The veteran multi-instrumentalist Ehrlich sticks mostly to alto sax for this one, an unusual choice in a trio. He plays tributes to Andrew Hill and Arthur Blythe, references that give a good idea of the inside-outside flavor of this excellent session. Ehrlich’s debut record, The Welcome, recorded some 40 years ago, was also a trio and is worth hearing too.

Chad Taylor – Smoke Shifter (2025). Another standout small-group jazz session with a timeless feel, simultaneously recognizable and fresh. The sax-trumpet-vibes frontline recalls some of the forward-looking Blue Note dates of the 1960s while being thoroughly contemporary (the WSJ review is nice). Taylor is also the drummer for in the unique trio Hears & Minds, alongside Jason Stein on bass clarinet and Paul Giallorenzo on synthesizers. Their latest album, Illuminescence (2025), mines some of the seams first opened up by Sun Ra, and unearths new treasures.

Augustus Pablo – King Tubbys Meets Rockers At 5 Cardiff Crescent, Washington Garden, Kingston (2025). A new collection of mostly unheard music from the great Pablo; it’s a sign of how productive the 1970s golden age of reggae was that there is still material of this quality out there. This collection of instrumental tracks is a stellar example of dub as vernacular avant-garde: the forms of pop music–three-minute songs performed on guitar, keys, bass, drums–are transmuted into mysterious slabs of rhythmic energy.

Ebo Taylor – Jazz Is Dead 022 (2025). The Ghanaian music legend recorded this new session with Adrian Younge and Ali Shaheed Muhammad at the age of 88; his voice is weaker than it once was but the beats are as compelling as always. Also now reissued and readily available are his early albums Ebo Taylor (1977) and Conflict (1980), true classics.

Jeff Parker – The Way Out of Easy (2024). Long, trance-inducing tracks selected from the years that Parker’s quartet played a regular Monday-night gig in L.A. Together they define almost a new genre of groove-oriented jazz that takes inspiration from other contemporary forms of beat music while staying improvisational and exploratory. Friends who don’t like much jazz like this.

Ben Goldberg – Here to There (2024). Another unusual horn-bass-drums trio: the clarinet is rarely heard in this exposed format. Goldberg and his trio mates Todd Sickafoose and Scott Amendola have an affinity for Thelonious Monk: their album Plays Monk from a few years ago was excellent, and this one extends the engagement, developing new tunes from bridges of Monk songs.

Seun Kuti – Heavier Yet Lays The Crownless Head (2024). The younger sun of Nigerian legend Fela Kuti, Seun Kuti inherited his father’s band Egypt 80, and much of his charisma and energy. I saw him on tour this year, and after a rocky start he delivered a stunning show. I like his new record a lot, the interlocking horn and drum parts are captivating as in the classic Afrobeat style, but the tunes more compact and focused.

Lee “Scratch” Perry x Bob Riddim – Destiny (2023). A posthumous collaboration between the legendary Perry and a younger producer. The last few albums Perry released before his death in 2021 were not very strong, but this one is fantastic, a more suitable capstone to his long career. On the record Perry has an old man’s voice, weak and quavery, but it somehow makes the songs even more intense and moving.

Charles Lloyd – Sangam (2006). Although I listened to a lot of Indian classical music this year, I didn’t put any on this list, as I still don’t really know how to talk about it. But I feel confident in saying this is one of the absolute best recordings of Indian-influenced jazz or jazz fusion. The interplay between the legendary tabla virtuoso Zakir Hussain and jazz drummer Eric Harland is tremendously exciting.

Craig Taborn – Light Made Lighter (2001). I may be a sucker for the horn-bass-drums trio, but I don’t love piano trios as much as a lot of other jazz fans seem to. This early effort by the amazing Taborn, though, is consistently interesting, one of the best contemporary piano trio records. I was turned on to it by Vinnie Sperrazza, in his appreciation of the work of drummer Gerald Cleaver.

Joe Lovano – Sounds of Joy (1991). Lovano’s first (but not last) trio recording, this often-overlooked album is an essential example of the form. The legendary drummer Ed Blackwell makes one of his last appearances on record with the two much younger musicians, Lovano on multiple reeds and Anthony Cox on bass.

Amina Claudine Myers – Song for Mother E (1979). Myers on piano and organ is accompanied only by drums on this unusual early recording, which doesn’t sound like anything else out there. The propulsive spiritual jazz of Alice Coltrane is one reference, though Myers is inspired more by gospel than Indian music. This album is now widely available for the first time in decades as part of the ongoing reissues of the catalog of Leo Records.

Miles Davis – On The Corner (1972). Like many jazz fans when On The Corner this record first came out, I just didn’t understand it the first time I heard it. What is this crap? I thought it was just bad funk. But when I went back to it this year, I could finally hear the music correctly. There are definitely highs and lows to Miles’ electric period, but this is one of the highs: dark and complex and intense.

John Coltrane – Expression (1967). When I saw Ravi Coltrane’s group this year, he closed the set by announcing he would play one of his father’s tunes, the title track of this album. It was a beautiful piece but I didn’t recognize it, and I thought I knew most of the late-period Trane. I had missed this one, his last studio recording, and a great session. Although some of the intense workouts of his group with Alice and Pharaoh can be unlistenable, here Trane is more focused and structured. It was a new direction that he never finished exploring: John would pass a few months later, when Ravi was only two.

Here are the most memorable of the books I read this year, listed in roughly the order I read them. It seems like reading 19th century authors was a theme in the culture this year, and I ended up participating in this trend without really planning to: Twain, Stevenson, Whitman were some of my highlights.

Fiction

Dashiell Hammett, Red Harvest. I re-read all of Hammett’s novels this year, and this, his first, held up the best. The later and better-known books seem more and more artifacts of their time: The Maltese Falcon is implausible and its plot famously incomprehensible; The Thin Man‘s clever repartee feels empty. Red Harvest has both a harsh portrait of the breakdown of state capacity and the effects of social violence (the setting is based on Butte, Montana) and a truly harrowing detective plot (the narrator suspects himself).

Mark Twain, The Adventures of Huckleberry Finn. I read this in tandem with Percival Everett’s James, which re-narrates the same events from a different perspective. Despite all the accolades for James, Twain’s original is, still, the better book. What is remarkable is how much the flaws and virtues of the two novels mirror each other: both start strong, with an immediately captivating narrative voice, and then fall apart at the end, as the characters perform unrealistic actions in service of some authorial conceit.

Samantha Harvey, Orbital. One of the most perfectly crafted pieces of prose I’ve ever read; short, basically plotless, almost unbearably intense. It is hard to call the book anything other than science fiction, since it is literally fiction about science, though it was mostly ignored by the genre community. Yet it succeeds more in evoking what used to be called the “sense of wonder” than most stuff in the genre does these days. Going to space is awesome.

Francis Spufford, Cahokia Jazz. A hard-boiled mystery set in an alternative 1920s America, by turns familiar and strange. Spufford is frank that he is imagining a utopia in which the Native American population was not erased by disease and thus could negotiate a political settlement with the European colonizers. But what gives the book its grit and charm is how messy and non-utopian his imagined mixed society is: prejudice, violence, and corruption persist.

Wallace Stegner, Crossing to Safety. How many novels are there that take as their main subject adult friendship? Stegner’s last, great work is an understated, closely observed portrait of the relationship between two couples. There are no affairs, and only the ordinary dramas of work and family. This year I also re-read his The Big Rock Candy Mountain, written more than 40 years earlier, which is an amazing but very different book: a more ambitious portrait of the character of America, or at least of one very American character.

Robert Louis Stevenson, The Ebb-Tide. Stevenson’s last published novel is not particularly famous but deserves to be better known. It came out in 1894, and the connecting line of inspiration and influence to Joseph Conrad, whose first book came out in 1895, is clear. There’s a South Pacific setting, a focus on interior psychology, a concern with colonialism. Scott Sumner thinks it might be Stevenson’s best novel.

Nonfiction

Robert Louis Stevenson, The Lantern-Bearers and Other Essays. Stevenson is best known as a novelist, but I think I prefer his nonfiction: he had an interesting life and was interested in lots of things, and the sentences are marvelous and daring. All of the essays are out of copyright and readily available online, but this is a good curated selection that is easier to manage. I picked out some of my favorite excerpts here.

Stuart A. Reid, The Lumumba Plot. Nominally a biography of Patrice Lumumba, this book is actually a gripping, blow-by-blow account of how the Congo stumbled to independence from Belgian rule. The events are tragic, not just for Lumumba but for the people of the Congo, who never really had a chance at being governed well. It’s a thematic and chronological sequel to Adam Hochschild’s earlier King Leopold’s Ghost, which documented the horrific excesses of Belgium’s colonial rule.

Perry Anderson, The Indian Ideology. Out of all the reading on India I did this year to prepare for my first visit, this was my favorite: compact, punchy, and argumentative, packed with erudition and information. I also enjoyed Anderson’s Disputing Disaster: A Sextet on the Great War, an investigation into the long-running argument over the causes of World War I through biographical sketches of historians. Not many writers have this kind of range.

Walt Whitman, Specimen Days. In his introduction, Whitman called this collection of his diaries “the most wayward, spontaneous, fragmentary book ever printed,” and it may still qualify for that distinction even 143 years after its publication. There is a lot of material from his visits to military hospitals during the Civil War; many long, quiet spells observing nature in southern New Jersey, as well as a journey out West. Tying them all together is Whitman’s love for the American landscape and people, and his unique voice, so fresh he still seems like a contemporary.

Joseph Henrich, The Secret of Our Success. One of the lessons I learned as a young student of anthropology is that culture is both subjective and objective: it exists in our heads, but also outside of our heads as a reality that shapes us. Henrich’s book is a remarkable effort to synthesize some of the core insights of anthropology with evolution and psychology (culture, or the “collective brain,” is the secret to humanity’s success). Not every plank in his argument is convincing, and the research has evolved since the book first came out a decade ago, but the ambition is impressive and the framework holds up.

Hampton Sides, The Wide Wide Sea. The last voyage of Captain James Cook is one of the more interesting and unique events in history: he was the first European to find the Hawaiian Islands and talk to the people there, and later, returning to the islands after mapping the coast of Alaska, was killed by them. The causes and meaning of those events have been debated ever since, and Sides delivers a careful, sympathetic and engaging account of the entirety of Cook’s final expedition.

Hu Anyan, I Deliver Parcels in Beijing (translated by Jack Hargreaves). Perhaps the best of the various gig-worker memoirs published in recent years. It’s less of a sociological document and more of a personal one, a story of how someone not well served by China’s educational system or job market gradually found a voice as a writer. (It’s interesting that none of the writers he mentions as inspiration are Chinese.)

Reading China’s five-year plans, one of the most immediately striking things is just how many things they attempt to plan. These are not just documents about where to build airports or highways (although such proposals do go into the plan). Recent iterations also cover many things that are not obviously amenable to top-down direction, such as what sorts of technological breakthroughs will happen in the future, and how social mores and customs will develop. In China’s Leninist political system, government attempts to specify the contours of “national economic and social development” are the norm rather than the exception.

In this context, restraint can be more notable than ambition. It’s not that surprising when plans declare extraordinary goals; it is more surprising when plans step back from attempted intervention. The 15th Five-Year Plan for the years 2026-30, now being drafted according to a set of “recommendations” approved by the Communist Party leadership in October, will certainly not be a laissez-faire document. Most mediacoverage has emphasized how the recommendations show China prioritizing industrial policy as it attempts to gain an edge in its geopolitical competition with the US. Here is a relevant section from the official English translation:

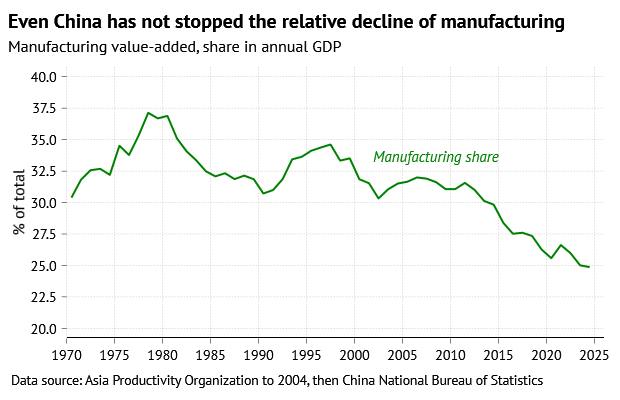

A modernized industrial system provides the material and technological foundations for Chinese modernization. We should keep our focus on the real economy, continue to pursue smart, green, and integrated development, and work faster to boost China’s strength in manufacturing, product quality, aerospace, transportation, and cyberspace. The share of manufacturing in the national economy should be kept at an appropriate level, and a modernized industrial system should be developed with advanced manufacturing as the backbone.

The obsession with advanced manufacturing as the avatar of the “real economy” is familiar from years of similar documents from China’s planning apparatus. But if we read this passage in the spirit of looking for what is missing, rather than what is included, one thing stands out: the language on the share of manufacturing. The 14th Five-Year Plan, when it was published in 2021, included a new goal to “maintain the basic stability of the manufacturing share” of GDP.

Previous plans had included goals to raise the service sector’s share of GDP, which at the time was seen as an indicator of the structural transformation and modernization of the economy. The 14th plan dropped those goals, and replaced them with the goal for stability in the manufacturing share of GDP. Rather than accepting that China’s economy would eventually look like everyone else’s–with the manufacturing share of GDP gradually falling over time–planners wanted China to stand out globally by avoiding the trend of de-industrialization.

It’s one thing to declare such goals, another to achieve them. The structural composition of an economy is not particularly easy to control: there is no single dial to turn that will boost manufacturing or scale back services. And in the event, the 14th plan’s declaration did not stop the manufacturing share of GDP from declining: it has gone from 26.6% in 2021, the first year of the plan, to 24.9% in 2024, and looks like it will tick down a bit more to around 24.8% by the end of 2025, when the plan period concludes.

This is not a large decline, and what counts “basic stability” is, after all, up to the government to decide. The Ministry of Industry and Information Technology, the agency responsible for this target, has already publicly declared that the manufacturing share is in fact basically stable. But the direction is clear: the manufacturing share of GDP has been in mostly uninterrupted decline since 2021. It spiked up during the post-Covid export boom of 2021, but has since resumed the downward trend.

The change in the wording for the next plan must therefore be read as an implicit admission of defeat: it was not actually possible to keep the manufacturing share of GDP unchanged, even with very generous subsidies for manufacturing investment and output. The next plan’s goal has thus been scaled back, from stopping the decline in the manufacturing share to just making sure the manufacturing share is “appropriate,” whatever that means. That this wording accepts some continued future decline in the manufacturing share of GDP was made clear in an explanatory article published in Seeking Truth, an official journal of the Communist Party leadership:

Traditional economics holds that a decline in the share of manufacturing and a rise in the share of services as the size of a country’s economy increases is a universal economic phenomenon. … The share of manufacturing in China displays an inverted U-shaped curve of “first rising and then falling,” which basically accords with the theory and practical regularities of industrialization. However, what we must be alert to is that this share must not decline too rapidly, nor fall to an excessively low level, as this could lead to serious consequences.

Among the main reasons that the manufacturing share of GDP tends to decline and the services share to increase in higher-income economies are that incremental household spending shifts from goods to services as incomes rise, and that changes in relative prices tend to make services (which tend to have slower productivity growth than manufacturing) a larger share of nominal GDP over time.

Both of these trends are a consequence of economic success, in terms of higher output and productivity: at least some of what is decried as “de-industrialization” is good actually. It is also good for China’s planners to recognize that reality and not distort the economy in pursuit of an impossible outcome. Obviously, a loss of export competitiveness would be a less positive reason for the manufacturing share to decline, but it makes more sense to focus on that issue directly than indirectly through an ambiguous indicator like the manufacturing share of GDP. Again, it’s not just significant what plans attempt to control—it is also significant what they do not attempt to control.

Will this change make a difference? Arguably, no. Since it’s not really possible for the government to directly control the relative shares of GDP of different sectors, it might not make much practical difference whether it has such stated goals. And there is still plenty of planning language about supporting the manufacturing sector. But it’s also arguable that changing the rhetoric will have effects. Technically, everything in the five-year plan has the force of law, and government officials are obligated to pursue the goals. The goal of maintaining the manufacturing share of GDP may have served as part of the justification for lots of specific policies that subsidized manufacturing output and investment.

There’s even a case to be made that those policies actually depressed the manufacturing share of GDP: by boosting output and capacity above where they would have been otherwise, subsidies probably contributed to the sustained decline in prices for China’s manufactured goods over the past few years, weighing on their share of nominal output. If subsidizing manufacturing output and investment is no longer so politically urgent, because there is no structural imperative to meet, then perhaps there will be room for those subsidies to retreat at the margin. That would certainly not be the outcome most outside observers expect from a five-year plan generally described as “doubling down” on industrial policy.

The first people you meet in life are your parents. That simple fact makes the family the foundational institution of society: learning how to be a person, and what other people are like, happens first in the family. After that, the next social institution most people encounter, in modern societies anyway, is usually schooling and education. Schools transmit social values to new generations, and help determine the specific social roles that the members of the new generations will occupy. Education is always a window onto society, and the new book The Highest Exam: How The Gaokao Shapes China, by the economists Ruixue Jia and Hongbin Li, is very illuminating on how China’s educational system has mattered for both social and economic outcomes, and on just why education is so important to so many Chinese families.

More profoundly than that, though, it makes a case for how one specific set of educational practices–the college-admissions exam known as the gaokao–serves as a fundamental structuring institution of contemporary Chinese society. Scores on the gaokao (or more precisely, the relative ranking of those scores) are the sole determinant of which students get admitted to which universities. Because college admissions are determined by gaokao scores–and nothing else, not recommendations or ability to pay–the test functions as a meritocratic channel for social advancement. There is fierce competition for the opportunity to attend the best colleges, but the competition is based on merit and merit is measured by exams.

In this basic structure, the gaokao is widely understood as the modern reincarnation of the keju, the imperial examination system that offered a chance, in theory, for any man in China to join the emperor’s civil service. The authors describe how millions wasted their lives in fruitless efforts to score high enough on the imperial exam to achieve a new and higher social status. But the fact that a meritocratic channel for social advancement existed was important; not having one seems to have, historically, not worked out well. The authors observe: “The exam system persisted for over a millennium, but after years of mounting criticism, the Qing government abolished it. Shortly thereafter, the Qing dynasty itself fell in 1911.” The ending of the exam system meant a huge loss of opportunity for the men who had spent years preparing for it, an experience that politically radicalized many of them.

When the Communist Party took over after China’s civil war, they moved quickly to reinstate a meritocratic channel for social advancement. The gaokao was first established in 1952, in the early years of the People’s Republic, as a nationwide exam that would identify talented young people for further education. The new leaders wanted a modern system for testing useful knowledge, not the ability to recite the Confucian classics, so the gaokao was a self-conscious modernization and reform of the old system. But the cultural memory of the keju was broadly positive: the population was already prepared to accept the idea that an examination system is, in fact, a fair way to identify merit. By associating itself with a traditional culture of exams and meritocratic advancement, the new Communist government gained rather than lost legitimacy.

The next Chinese leader foolish enough to mess around with exams was Mao Zedong, who during the Cultural Revolution shut down the gaokao, along with the normal functioning of the entire educational system. The Cultural Revolution for a while turned meritocracy on its head, punishing the educated classes and elevating workers and peasants. Universities did eventually resume classes, but they were mostly about ideology, and admissions were done on the basis of political recommendations. But Mao’s death opened the floodgates, and the leaders in Beijing were inundated by protests and petitions demanding the reinstatement of the gaokao. Although the start of China’s “reform era” is conventionally dated to 1978, when some top-level political meetings were held, some people consider the real start to be 1977, when Deng Xiaoping restored the test and univerisites admitted a new class of students selected on the basis of academic merit.

One possible reading of the last century or so of political history in China, therefore, is that governments who provide a meritocratic channel for social advancement have legitimacy and popular support, and governments who do not provide one, do not. Such a pattern may have held in previous centuries as well: one of the co-authors’ many papers summarized in the book quantifies how the introduction of the keju system, around the 7th century AD, reduced Chinese emperors’ risk of being dethroned by a factor of 10. Certainly, the way more recent governments have behaved suggests they think the gaokao helps keep them in power. The gaokao is not seen as legitimate because it is instituted by the Communist Party; rather, it is the Communist Party that gains legitimacy by administering the gaokao in an even-handed way.

That’s not to say that the exam system is without downsides. For all of its popular support, the gaokao creates an incredibly high-pressure social environment. It’s not just that there’s one test that everyone has to take, but that children’s entire educational trajectory is built around preparing for success on that test. The gaokao is just the culmination of a series of tests and sorting procedures that choose who will be admitted to China’s elite universities, which to a remarkable extent determines who will be in the social and economic elite. Parents work relentlessly to position their children to do well on the gaokao, because, literally, nothing else matters; there are essentially no alternative pathway to success in Chinese society. Because people arrange their entire lives to help their kids succeed on the gaokao, changes can threaten the investments already made, and lead to strong resistance.

In 2013, according to the book, Hongbin Li was asked by China’s government to design a replacement for the gaokao. The initial idea was to switch out the single all-important test administered on only one day for a series of tests in different subjects, which could be taken multiple times throughout a student’s high school career–somewhat analogous to the Advanded Placement (AP) tests in US high schools. That probably would be less stressful for students, and make for a fairer assessment of their achievements. Li designed textbooks and tests and even started training teachers in the new approach, before the whole effort was scrapped. Even smaller changes to the gaokao system to try to address entrenched inequality had generated surprisingly widespread political protests, and been quietly walked back. The impression is very much that the exam system amounts to an untouchable “third rail” of Chinese politics.

One of the more interesting implications of the book is that because the social prestige of the gaokao is so high in China, and because everyone has been trained to understand and work with that kind of system, that it has implicitly become the model for other social institutions outside of education. The authors analyze the underling structure of the gaokao as a “centralized hierarchical tournament”: the competition between students is centralized because there is only one standard of success, and it is hierarchical because success is defined in relative terms, by doing better than those around you. Once the concept is grasped, it is easy to see many other centralized hierarchical tournaments in Chinese society.

The most consequential of these is probably the competition among local governments to generate economic growth, which many scholars have identified as one of the fundamental structures underlying China’s reform-era growth boom. Local officials are always competing for promotion and advancement, and one of their key performance indicators is economic growth in their jurisdiction. That competition is centralized because there is, effectively, only indicator of success, GDP growth, and only one arbiter of success, the central Party apparatus. And it is hierarchical because success is defined relative terms: it’s about where is your GDP growth relative to your peers and predecessors in office.

That system makes sense for some of the same reasons that the gaokao does: GDP growth, like an exam score, is a relatively objective and transparent metric, better than many alternatives. Also, centralized hierarchical tournaments seem to be good at creating very effective incentives. The competition among Chinese students to do well on the gaokao does in fact result in most of them acquiring real skills and knowledge. And the competition among local governments has in fact delivered a lot of GDP growth.

The centrality of the gaokao, and gaokao-like institutions, in China makes it all the more intriguing that the man now sitting on top of the political system seems less committed to them than many others. Xi Jinping belongs to the last generation of “worker-peasant-soldier” students admitted to university on the basis of political recommendations rather than exam scores. (This wasn’t an automatic result of his being the offspring of a senior Party leader. Joseph Torigian has documented that because Xi’s father had been purged during the Cultural Revolution, his initial applications to university starting in 1973 were rejected; but eventually a sympathetic administrator approved his admission.) This has always set Xi apart from other more “technocratic” figures in the government, like his former No. 2 Li Keqiang (see my old post on “The education of Li Keqiang“).

Xi famously oversaw the shuangjian or “double reduction” campaign launched in July 2021, which aimed at easing the “burdens” on students of excessive homework and after-school tutoring–one of the most high-profile attempts to address the downsides of the gaokao system in recent years. This got a lot more attention outside China than most such political campaign, because it essentially outlawed the business model of some publicly traded companies. While the rules remain on the books, recent evidence suggests that enforcement has been relaxed, and businesses are again being allowed to meet parents’ demand for tutoring, which remains very high. The exam system remains a fundamental social institution of today’s China, and as such very difficult to change.

Two things happened this year to convince me to do some more intentional listening to Indian classical music, which I had long been aware of but had never really “got.” The first was the untimely death of Zakir Hussain, the beloved tabla virtuoso; he had been scheduled to play a concert near where I live and I thought I would finally take the opportunity to see him in person. Now I will never have one. The second, also unexpected, was an invitation to go to India for a conference, which would be my first time to visit. It seemed like a sign.

So, on a day off in Delhi, I paid a visit to Radio & Gramophone House–a 74-year-old record shop and one of the last remaining, Indians like everyone else having gone mostly to streaming. I asked them for an introduction to Indian classical music, instrumental not vocal, and the friendly gentlemen set me up with a bag of CDs to take home; I was only sad I could not carry some of the marvelous LPs they had. (If you’re in Delhi, please give them some business.)

The wares at Radio & Gramophone House in Delhi

Since then I’ve been working my way through that initial stack of CDs, supplemented by some other purchases and downloads and re-listening to things I already had but to which I had not paid proper attention. It’s been very worthwhile. If, like me, you appreciate the improvisational flights and rhythmic delights of jazz, then Indian classical music will not seem very foreign for long. The best bits are marvelous, without question. But it is a daunting edifice from the outside, and it is hard to know how to approach. Here are some of my initial thoughts on what is so great about Indian classical music, and how to get into it as a curious outsider.

You can think of music as having four axes of variation: melody, harmony, rhythm, orchestration. The structure of Indian classical music downplays two of these: there is no harmony, and the orchestration is minimal, with usually only one melody instruments and one or two accompanists. It’s all melody and rhythm, but these are intensely investigated. To the Western-trained ear, the lack of harmonic progression can make the structure of the music difficult to grasp, and is why people sometimes complain that it “all sounds the same.” It takes some repeated listening to hear what is there rather than what is not.

Another barrier is a more pratical one: most pieces of Indian classical music are long. Particularly in the northern, Hindustani style best represented on record, tracks rarely come in under twenty minutes, with full performances of a single raga easily reaching an hour or more. I like variety, so if I have an hour to listen to music I would usually prefer to listen to several different pieces rather than just one. Even for really great jazz players, I rarely want to listen to those forty or fifty minute jams. Improvisers can be prolix and reluctant to edit themselves, but for listeners shorter is usually better. For these reasons, I found some of the classic recordings from the LP era (mostly the 1960s) to be good places to start with Indian music. The constraints of the medium keeps the length of the pieces relatively contained, and that constraint is actually a benefit.

So if, to the Western ear, Indian classical music initially seems kind of long and boring, what is the attraction? It’s often marketed to Westerners as a kind of functional music for the spiritual lifestyle, accompaniment for meditation or whatever. The drones and the slow pace of the opening sections of the ragas contribute to this vibe, and it’s true you need a little patience to get started. But this is not what I’m after at all. The good stuff is actually quite exciting, with the interplay between the long melodic explorations and the intricate rhythms delivering some of the same joys that other improvised music does, while still being very much a distinct tradition.

The tabla. Percussion is really at the heart of Indian classical music, and while there are other percussion instruments, for now I’m still most in love with the sound of the tabla. Zakir Hussain is amazing and had a long and productive career; a reasonable algorithm for finding good recordings of Indian classical music is just to look for ones that he plays on. The Bandcamp page of his personal record label has a lot of good classical recordings, as well as many of his other efforts. (He also did a lot of fusion and cross-genre work, which I have not explored so much; honestly I haven’t loved what I’ve heard of Shakti, the band he was in with John McLaughlin).

His father, Alla Rakha, was also a tabla master and played on many classic recordings from the 1950s on; again, you could do worse than to just seek out recordings with his name on them. Both of them made solo tabla recordings, and even a few tabla duets together; I’ve sampled these but I think I’m not an advanced enough listener to really appreciate them, it’s not where I would start. Another major tabla player, recommended by the Radio & Gramophone House guys, is Shankar Ghosh.

The sitar. The chiming of the sitar’s multiple resonant strings is perhaps the most immediately identifiable sound of Indian classical music. It’s hard to avoid the sitar or Ravi Shankar in a survey of the recordings easily available outside India, and really there’s no reason to. I like his early Ragas & Talas LP, from 1959, and the other 1960s recordings are pretty good too. Other amazing sitar players are Nikhil Banerjee and Budhaditya Mukherjee, and it is easy to find lots of their work on streaming services.

The sarod. The best Ravi Shankar, however, might just be his collaborations with the sarodist Ali Akbar Khan, a towering figure in the music. Possibly the first example on record is this track from 1955, on a UNESCO compilation available through Smithsonian Folkways, but they kept playing together for decades. Their duets (known as jugalbandis) are some of the real high points of the genre; the call-and-response is delightful.

The sarod and sitar sound great together, but I discovered that I actually prefer the sarod: an instrument of the lute family, its sound is a bit deeper, more forceful and direct, highlighting the melody more. Ali Akbar Khan’s work is amazing and should be sought out; some other major sarodists are Sharan Rani, Amjad Ali Khan and Aashish Khan. Again, a wealth of marvelous material from all of them is available on streaming services. One individual recording I would highlight is the collaboration between Ali Akbar Khan and Nikhil Banerjee released on Khan’s own label as Signature Series Vol. 4; it’s widely recognized as a stone-cold classic.

Other instruments. The bansuri, the Indian side-blown bamboo flute, is another common lead instrument, but I don’t love it as much as the sarod. The most famous practitioner is Hariprasad Chaurasia, who is prolific and widely beloved. I quite enjoyed some of his recordings, but found others to be a bit soporific. The double-reed instruments, shehnai and nagaswaram, for me are hard to appreciate.

One of the interesting things about Indian classical music is how much innovation in instruments there has been: many Western instruments were adopted and modified by Indian musicians in the 20th century to play in the Indian classical style. For instance, there are now many violin players in the tradition, but I haven’t listened to them much yet so don’t have much to suggest. Bringing in new instruments has generally worked very well: modern instruments generally have more reliable tone, wider range, and better projection than traditional instruments–they are better as instruments.

One well-known figure is Vishwa Mohan Bhatt, who invented his own instrument, the mohan veena, a kind of cross between a guitar and the veena family of stringed instruments. He won a Grammy for his collaboration with the roots guitarist Ry Coorder; it’s a nice-sounding record but frankly his work in his own tradition is much better, and very rewarding. Again, there is lots on streaming.

Brij Bhushan Kabra, a student of Ali Akbar Khan, played a modified slide guitar, which sounds fantastic as an Indian classical instrument; I found a nice LP reissue of his 1982 record with Zakir Hussain. Kadri Gopalnath brought the alto saxophone into the southern, Carnatic tradition, and he is amazing too. Jazz listeners might be more interested, but really he sounds nothing at all like jazz. He has a unique sound but is not perhaps the best introductory listen for tuning your ears to the particular beauties of Indian classical music. For that I would go first to Ali Akbar Khan.

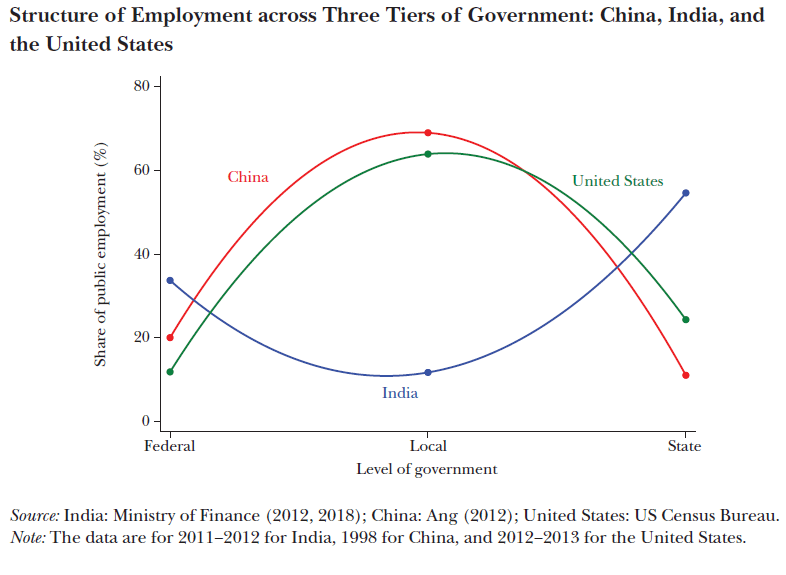

After doing a round of India-China comparisons that focused on commonly cited macro indicators like manufacturing, investment and literacy (see last month’s post “India and the invidious comparison with China“), I wanted to highlight a lower-profile but perhaps even more interesting contrast: the structure of government and the nature of decentralization in large countries. One of the coolest China-India charts I have seen is in a 2020 article in the Journal of Economic Perspectives by Devesh Kapur, “Why Does the Indian State Both Fail and Succeed?” It shows how public employees in India, China and the US are distributed across different levels of government:

Notably, India has many more of its public servants at the state level than China does at the equivalent provincial level, and many fewer at the local (i.e. cities and towns) level than China does. (The China numbers come from an interesting paper by Yuen Yuen Ang; the data sources unfortunately stop in 1998). On this measure, state capacity at the local level looks much stronger in China than in India, which helps explain some of the long-running economic differences between them. (The structural similarity of China and the US in public employment is also pretty interesting!)

Some of the major indicators of India’s poor state capacity are its failures in delivering public services like health and education, which happen at the local level. China does much better in basic service delivery–and its local governments have also played a very obvious and important in driving growth, thanks to the competition and experimentation among local officials driven to develop their jurisdictions. That process presumes a certain baseline level of state capacity and autonomy at the local level, which may be harder to come by in India.

Why is the structure of government authority distributed so differently in Asia’s two billion-person continental-scale civilization-states? History. Karthik Muralidharan’s definitive book on state capacity in India, Accelerating India’s Development: A State-Led Roadmap For Effective Governance, says that questions of federalism and devolution greatly occupied the drafters of India’s constitution at independence. Despite the claims of nationalist propaganda, India had not been a unified state prior to British colonialism, and was not really a unified state under British rule. The leaders of the new country quite reasonably did not trust local authorities enough to give them great autonomy:

The political reason [for centralization] was the concern that post-British India would not remain unified, a fear amplified by the Partition of the subcontinent into India and Pakistan. Further, at the time of Independence, more than 40% of India’s land was ruled by over 500 erstwhile princely states, whose rulers had only recently acceded to the Indian Union, and some had done so quite reluctantly.

To understand the enormity of the challenge of uniting the nation, some historical context is useful. In the 2000 years before British rule, even 75% of the Indian subcontinent was politically unified for less than 200 years: under the peaks of the Mauryan and Mughal Empires (around 300-250 BCE and around 1600-1700 CE). So, preserving national unity was a top priority for the Constitution’s framers. This is why they gave the Central government strong political powers, including the ability to dismiss democratically elected state governments under Article 356.

The national elites designing independent India’s political structure also did not trust the traditional elites at the local level to share their social and economic agenda. They did not want to give local governments lots of authority over money and social programs, because they knew the traditional local power brokers would inevitably influence government for their own benefit:

The lack of autonomy of lower tiers of government reflected the concern that local elites would seek to perpetuate patriarchy and caste inequalities, through actions such as denying or limiting education to girls and disadvantaged castes, if they were given power over local service delivery. This lack of trust is perhaps best captured in the famous words of Dr. Ambedkar, ‘What is the village but a sink of localism, a den of ignorance, narrow-mindedness and communalism?’ …

Though the first principles of federalism suggest that local government should be responsible for service delivery, India’s approach to designing a federal governance system has been much more centralized than almost any other country in the world. A key reason for doing this was to have a professional state-level bureaucracy that could implement government policies and programmes to benefit disadvantaged groups, that may have been resisted or even thwarted by local elites.

Why have China’s political leaders been more confident that they could devolve some authority to local governments? They definitely cared a lot about national unity, but fissiparous tendencies were perhaps less of an immediate risk after the Communist Party’s victory in the civil war. China did have a longer history as a unified state (the boundaries of the People’s Republic of China are largely the same as that of the Qing Empire), and the fight against the Japanese invasion in the 1930s had helped forge strong popular nationalist sentiment.

The new Communist state in China was also just much more ruthless in ripping out traditional social structures and replacing them with its own lines of command. First there was the land reform in the 1950s that dispossessed and killed millions of local gentry. Later the Cultural Revolution eradicated many of the remnants of traditional society, as the nation was consumed with campaigns to tear down any source of authority other than the Chairman. Mao himself always favored local initiative and autonomy, at least rhetorically, but this assumed a framework of uniform nationwide loyalty to the Party. The Cultural Revolution’s relentless political campaigns also ended up destroying much of the ability of China’s new bureaucracy to function. Yet when the post-Mao leaders started rebuilding state capacity, they would have faced less competition from traditional social structures.

I recently wrote a piece at my job, and somewhat unusually for us, it’s come out from behind the paywall so that everyone can read it. Here’s the opening:

There are two statements about China’s economy that receive broad agreement today. One is that China faces a long-term structural slowdown in its growth rate, due to a laundry list of factors including the law of large numbers, changing demographics and less catch-up potential as an upper-middle-income country. The other is that China’s economy has recently been underperforming, suffering from extended deflation and weak employment, and would benefit from more aggressive cyclical stimulus. It’s not contradictory to believe both of these things, but there is some tension between them.

The way people resolve that tension is, at least implicitly, by taking a view on the output gap–the difference between actual economic growth and its underlying potential. If you believe more strongly in the structural slowdown story, then you think the output gap is unlikely to be large, as the economy’s potential growth is steadily declining. If you believe more strongly in the current underperformance, then you think the output gap is large, and needs to be addressed. What’s curious is that while China’s government professes to believe that the potential growth rate of the economy is high (thanks to all of its wise industrial policies), it doesn’t act that way.

Whatever their expressed views might be, China’s policymakers are not acting as if they believe there is currently a big output gap. While fiscal stimulus has stepped up in 2025, the support from monetary- and property-policy measures has been less than expected. Official rhetoric is increasingly treating deflation not as a sign of deficient aggregate demand, but as a structural problem best dealt with through regulatory changes and industrial policy. Such interventions have stepped up since the July meeting of the Central Commission on Financial and Economic Affairs, chaired by top leader Xi Jinping, said the government would “regulate and manage disorderly low-price competition among enterprises in accordance with laws and regulations.”

Despite some public differences, it seems that both Chinese government officials and the staff of multilateral institutions hold fundamentally similar views: they believe more strongly in the structural slowdown of the Chinese economy than in the contemporary evidence of a large output gap. Financial-market participants, by contrast, tend to hold more strongly to the view that more aggressive stimulus is necessary.

I’m with the markets here: I believe in the output gap. The structural slowdown of the Chinese economy is an incredibly consensus view, and I believe in it too. But for a variety of reasons I think it makes more sense to stay agnostic about forecasts of potential GDP growth, and focus more on the signals the current performance of the economy is sending.

Around my trip to India I did some not-very-systematic reading, and had pretty good luck. All of these books were worth reading and helpful in different ways:

Perry Anderson, The Indian Ideology (expanded second edition, 2021). Anderson’s range of erudition is impressive–I read this book after finishing his latest, Disputing Disaster, a deep dive into the historiography of the First World War–and he packs a lot of information into his short, polemical account of Indian politics. The book’s aim is to destabilize what he calls the mainstream narrative of India’s liberal intelligentsia: the celebration of a stable, secular, multicultural democracy. He re-examines key episodes in India’s independence struggle and early history to emphasize the enduring roles of religion, caste and social division.

Rukmini S., Whole Numbers And Half Truths: What Data Can And Cannot Tell Us About Modern India (2022). This book by a data journalist is written to explain India to Indians, not to explain India to foreigners, which makes it more useful and interesting. Some background knowledge is required–you need to know what scheduled tribes are, things like that–but it is clearly written and informative, covering topics from crime to marriage to diet. Her mode is patient, careful explication, going as far as the facts allow and no further. Nevertheless she aims her darts to puncture some of the same liberal illusions targeted by Anderson, broadly arguing that India is fundamentally a conservative society where caste, class and religion are dominant concerns, not a primarily secular one organized around economic interests.

Ashoka Mody, India Is Broken: A People Betrayed, Independence To Today (2023). Another polemic (does India just inspire polemics?) structured as a detailed history of Indian politics and economic policymaking. Mody’s overriding concern is India’s failure to get onto the East Asian trajectory of export-led manufacturing, and he wants to identify the specific points where it went astray. He puts the blame on two main factors: the failure of the educational system to deliver broad-based improvements in human capital across the population, which is convincing, and the repeated failure of the government to devalue the currency to achieve export competitiveness, which I found less convincing. While hardly impartial, the book is effective in showing how poorly served India has been by its political leadership, and details well the bad decisions and corruption.

Karthik Muralidharan, Accelerating India’s Development: A State-Led Roadmap For Effective Governance (2024). A very long book, which I have not yet finished but can still highly recommend. It’s probably one of the best books ever written on state capacity, working steadily and patiently through all of the aspects of the weakness of the Indian state, and proposing reasonable and technical fixes. This is another book written for an Indian audience, so there is more micro detail than all outsiders will want, but it is just this forensic examination of the functioning of state institutions that is so valuable. There should be a book like this for every country–in particular the US, which is also facing its own state capacity crisis and needs this kind of engagement with the realities rather than the theories of governance. The book’s bias is more in the underlying assumption that technical fixes are possible, though he acknowledges that some of the social and political problems identified by the other authors on this list contribute to poor state capacity.

In June I went to India for the first time. It was a quick trip, just a week, but I still got a pretty intense introduction to current debates on the Indian economy at the India Policy Forum in Delhi. As a China specialist with only a newspaper-reading level of familiarity with India, I was quite intimidated by the prospect of joining a roomful of people who have spent their entire lives working on tough economic questions of India. It turned out, though, that if you’re going into the equivalent of a high-level graduate seminar on Indian economics as an outsider, having a background in China is not the worst preparation. Almost every paper and every talk about India’s economic problems seemed to be motivated by some implicit comparison with China.

At first I thought I was over-interpreting things because I am biased to look at things from a China perspective, so I asked around to check my perceptions. The answer was: Yes, all this is in fact about China. It’s because the Indian elite has assumed for decades that India is destined to be the next global economic superpower after China, so the overriding question for them is why that hasn’t happened and what needs to be done to make it happen. The comparison with China seems to revolve around a number of generally accepted stylized facts, which form the basis for identifying policy issues and posing research questions. To me (as, again, an outsider to these debates), the key ones seemed to be around manufacturing, investment, human capital and state capacity.

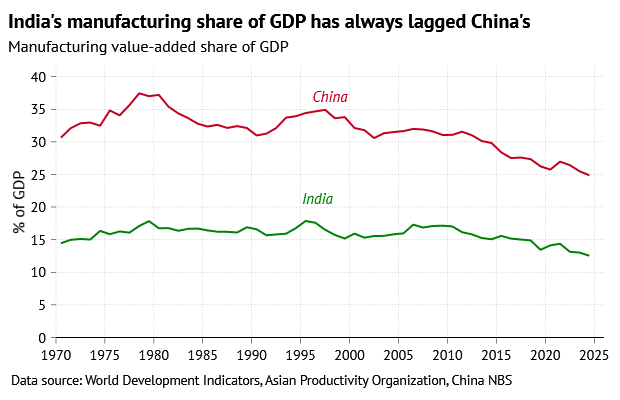

One of the most obvious economic contrasts between India and China is that China has followed the East Asian model of export-led manufacturing, like Japan, South Korea and Taiwan (albeit at much greater scale), and India has not. All of those Asian economies historically had high manufacturing shares of GDP, and while in all of them the manufacturing share is lower today, it is still higher than in India. In recent years India’s manufacturing share of GDP has been around 13%, about half of the level in China, and historically it has never exceeded 18%. One of the central debates among Indian economists is how much of a problem the relative weakness in manufacturing is, and what should or could be done about it.

Historically, it is definitely true that manufacturing has been a key motor for structural transformation away from traditional agriculture to modern production based on wage labor and economies of scale. And the reason many Indian economists worry about the low manufacturing share is that it seems to be a symptom of slow structural transformation: the agriculture share of GDP and employment has remained largely static in recent years. So while the modern sector in India’s economy is clearly growing, it doesn’t seem to be pulling workers out of the traditional sector, limiting the income gains. That concern is behind proposals to encourage the growth of labor-intensive manufacturing.

India’s government has also set explicit targets for the manufacturing share of GDP: the “Make In India” initiative back in 2014 called for pushing up the manufacturing share to 25% by 2022, which obviously didn’t happen. NITI Aayog, the public-sector think tank that has replaced the old Planning Commission, is still talking about a 25% target, this time for 2047, the centenary of India’s independence. It is worth noting that China has, in fact, never set a quantitative target for the manufacturing share of GDP. Currently the government just talks about “maintaining basic stability” in the manufacturing share, which hasn’t stopped it from declining.

It’s also interesting that a recent comparative study of China, India, Indonesia, Mexico, and South Africa emphasizes that transitions out of agriculture played a limited role in raising household incomes out of poverty; income gains within sectors often played a larger role than reallocation among sectors. Which is not to say that more structural transformation of the economy would not be helpful for India, but perhaps it is not right to get hung up on the relative shares of different sectors. After all, there’s no economic theory that can tell India what its optimal share in GDP of manufacturing should be. You can’t treat shares of GDP like temperature readings, and use naive cross-country comparisons to say, oh, this level is obviously too low, there’s a deficiency, or this level is obviously too high, there’s an excess.

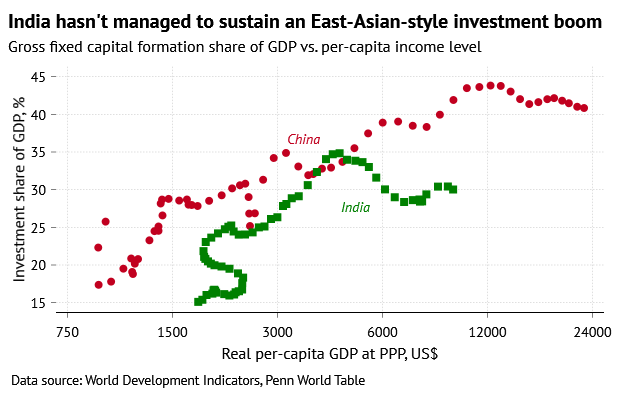

A closely related contrast between India and China is its relatively lower investment share of GDP. One assertion I heard, which received broad agreement, was that no country has been able to successfully develop without sustaining an investment share of GDP of over 30% for decades. This is based on the East Asian development experience: Japan, South Korea and Taiwan, as well as Malaysia and Singapore, all sustained 30%-plus investment rates for long periods of time, alongside their higher manufacturing shares of GDP. China of course, is the investment champion, for better and for worse, keeping its investment share of GDP consistently over 30% since 1992, and over 40% for the past 15 years. Again, China is implicitly (and often explicitly) the point of departure for the Indian debate. A World Bank report this year endorsed a “reform” agenda to push India’s investment share of GDP to 40% by 2035.

India’s investment share of GDP is actually not that low: it’s been around 30% in recent years, and was over 30% for roughly the period of 2005-13. True, this does not quite meet the (perhaps arbitrary) historical threshold for an East Asian-style investment boom. And some Indian economists express concern that the recent pickup in investment is aided by large public-sector investment in infrastructure, which may not be sustainable, and that private-sector corporate investment has been static or falling as a share of GDP. While corporate profits have been strong in recent years, they report that the weakness of private-sector investment seems to be concentrated in manufacturing: companies just do not see good prospects for adding manufacturing capacity. If India does not have a manufacturing boom, it probably will not have a broader investment boom.

An alternative view expressed by some other economists is that India is already growing rapidly with a 30% investment rate, the current returns on services investment are high, and it’s not obvious that it needs to push a lot more investment. I found myself sympathetic to this side of the debate. China today, after all, is hardly a model to follow: it has experienced massive excess capacity and declines in returns on capital since the 2008 global financial crisis, largely due to forced public-sector investment.

Still, China’s current excess investment is a product of both its peculiar quasi-socialist institutions and particular historical circumstances, neither of which have very close analogues in contemporary India. If India can find productive uses for a few more percentage points of GDP worth of investment, that would probably be welcome, and would hardly put it on the path to Chinese-style excess. But equally, it’s hard to take a simple cross-country comparison as sufficient justification for massive macroeconomic interventions to push up the investment share.

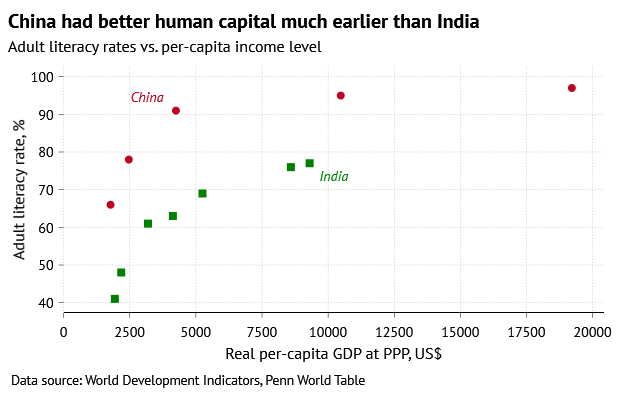

A more supply-side perspective on India’s relative dearth of manufacturing and investment focuses its failure to establish the necessary social preconditions for an East Asian-style growth takeoff. As Wang Feng’s recent book China’s Age Of Abundance emphasized, China was able to seize the opportunity presented by labor-intensive export manufacturing in the 1980s because it had made substantial improvements in health, education and gender equality in prior decades. China’s workforce already had the necessary human capital to transition effectively to jobs in the modern economy, when reforms started to make those jobs available.

In terms of some basic measures of human capital, India has yet to catch up to where China was decades ago. According to the World Bank, India had an average adult literacy rate of just 77% in 2023–roughly China’s level in 1990. This average gap is aggravated by the scandalously low female literacy rate in India, just 70%. (Other measures like average years of schooling also show a gap). One reason why manufacturing has not taken off in India may well be that India does not have a mass workforce equipped with the basic skills to perform manufacturing jobs.

The low average endowment of human capital in India is striking given the high achievements of the most educated: India obviously does have a workforce equipped to perform high-skilled jobs in information technology and services. A recent paper by Nitin Kumar Bharti and Li Yang collects a remarkable amount of historical data to show substantial differences in educational priorities between India and China. After independence, India invested more in university education but neglected primary and secondary education, producing a relatively small cohort of skilled graduates amid a large uneducated and illiterate population. China, by contrast, initially focused on achieving broad-based basic education before emphasizing the expansion of university education after the 1980s.

Bharti and Li document that India has since the 1990s tried to expand enrollment in primary and secondary education, which is reflected in rising literacy rates. But the quality of basic public education still seems poor, and more education spending is not always producing better results. There are lots of shocking stories about widespread teacher absenteeism and incompetence. It is generally reported that higher-income Indians will do whatever they can to stay out of the public education and healthcare systems. This points to an even more fundamental contrast between India and China, which is in state capacity: the government’s ability to get things done.

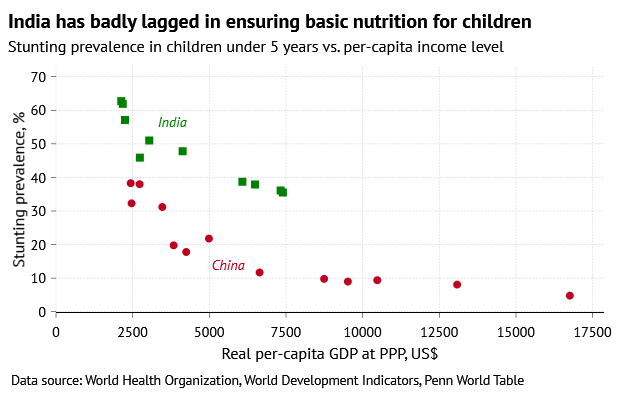

In particular, India’s government seems to struggle to deliver basic public services and provide a baseline level of human welfare. Another fact about India that is, deservedly, often repeated is its alarmingly high proportion of underweight and stunted children. The last survey data collected by the World Health Organization show that 36% of young children in India were stunted (far too short for their age) in 2020. That’s similar to the proportion in China in the mid-1980s; but China at the time had per-capita GDP of only a third of India’s today. An interesting case study of Karnataka, one of India’s most developed states and home to the IT hub of Bangalore, reinforces the point. While Karnataka has had one of the best growth stories in India, it has still a higher proportion of children who are stunted, underweight or not enrolled in school than some poorer states. The significant increase in economic resources available to the state government does not seem to have translated into better outcomes for much of its population.

One set of these comparisons and stylized facts, those on manufacturing and investment, are frequently used to argue for more aggressive efforts to transform India’s economy and put it on something more like a Chinese (or East Asian) trajectory. But the other set of comparisons, on human capital and state capacity, implicitly counsel caution. If India does not have the necessary preconditions for a manufacturing takeoff, companies probably would not respond strongly to government favoritism for manufacturing (and indeed most people seem to think the response to the Make In India initiative has been underwhelming). In any case, a government that struggles to deliver basic public services is unlikely to be able to execute interventionist industrial policies effectively. Even China has plenty of waste and corruption scandals alongside the success stories.

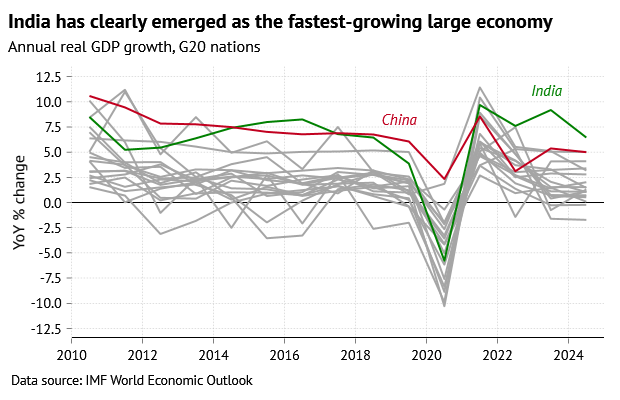

Yet it is also worth emphasizing that India does not come off the worse in all comparisons with China. It’s an important fact that, since the pandemic, India has overtaken China to become the world’s fastest-growing large economy, averaging real GDP growth of over 7%. This is all the more remarkable given that India clearly is not having an East-Asian-style boom in manufacturing and investment. Therefore, it must be having some other kind of boom: one led by services. The IT outsourcing wave, which got started in 1985 when Texas Instruments opened a research center in Bangalore, seems to have stepped up to a new level in the last few years, possibly boosted by the post-pandemic changes in working patterns. Foreign investment clearly plays a big role in this process, and I saw huge swathes of new office parks going up outside Delhi, adorned with multinationals’ names.

Given that, by general consensus, India has not solved its outstanding problems in agriculture and manufacturing, the fact that the services boom is strong enough to power 7%+ aggregate growth is pretty impressive. It’s hugely important that India now has a self-reinforcing growth cycle in foreign and private-sector investment and exports. It’s almost reminiscent of what happened in China in the 2000s after its WTO entry, even if India’s cycle is mostly in services, which have fewer spillovers to the rest of the economy than manufacturing. If there is an alternative school of thought to the one focused on trying to “be like China” in terms of macro aggregates, it is that India should focus on building on what is already working. That means not just facilitating the tech boom, but also making more sectors outside IT services attractive to investment from both domestic and foreign businesses, and trying to steadily improve state capacity and public services.

Incremental reforms might be more politically realistic than trying to drive a “big push” in manufacturing investment. Most of the commentary I heard in Delhi was pessimistic about the outlook for big policy changes, since the current fast GDP growth sends a signal that things are going well, and makes disruptive and politically costly reforms seem less necessary. But it is also true that evidence-based comparisons with China should be able to motivate lots of different ideas about what India can do: China itself has gone through lots of changes, and the growth model has been quite different at different points in time. There are a lot of people these days who think “being like China” means “doing manufacturing-heavy industrial policy,” but this is a perspective distorted by the particular set of government priorities since 2015 or so.

China’s turn to aggressive industrial policy came only after it had already become a quite successful export manufacturer. And that turn was explicitly justified on grounds of national security rather than promoting growth. It was precisely because China was already quite developed that it could afford to put lots of money into import substitution and speculative technological bets. The industrial-policy apparatus of today’s China is a completely inappropriate model for India, which faces a very different set of problems with a different set of capabilities. A focus on removing impediments to a private-sector-led expansion would in fact make India more like China–just the China of a different, less statist era.