Just what can we realistically expect in terms of state-owned enterprise reform in China?

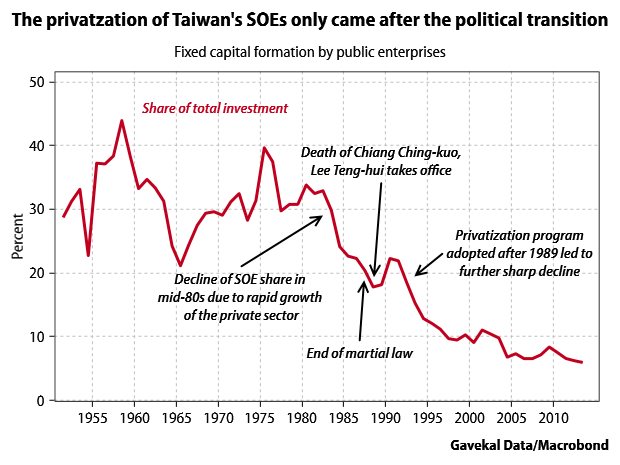

For those who take the once-standard view that China is following the “Asian developmental state” model of Japan, South Korea, and Taiwan, then substantive SOE reform and privatization should in fact be coming along any day now. Those other Asian economies also had large state sectors originally; Robert Wade’s 1990 book on Taiwan, Governing The Market, notes that “from the early 1950s onward Taiwan has had one of the biggest public enterprise sectors outside the communist bloc and Sub-Saharan Africa.” Wade defended the performance of Taiwan’s SOEs, but his book was published just as a major privatization program was pushed through. Taiwan, rather unusually, has good and transparent data about the size of SOEs in its economy, which makes for an interesting chart:

South Korea had an SOE sector whose relative size was not that dissimilar from Taiwan’s, and actually began privatization even earlier. I have cobbled these data together from a few different sources, so I wouldn’t pretend to a huge amount of precision, but the trend is still pretty informative:

Major privatizations of SOEs in South Korea took place in the early to mid-1980s, when its per-capita GDP was $7,000-$9,000 at purchasing power parity. Taiwan’s privatization came later and at substantially higher incomes, around $17,000-$18,000 at PPP. China’s per capita GDP is around $13,000-$15,000 now. So if we’re just thinking in terms of income levels, China is more or less at the point when substantial SOE privatization happened elsewhere. But income levels are pretty obviously not the driving factor; SOE privatization in both South Korea and Taiwan was very much part and parcel of their political transitions toward democracy. And such a transition does not seem to be at all imminent in China.

A couple of conclusions seem to follow from this observation. One, the “Asian developmental state” framework, which was indeed helpful for analyzing China in its high-growth phase, seems to be outliving its usefulness. A different perspective that takes China’s socialist heritage more seriously, perhaps looking more at transition economies, could be useful. Two, expectations for SOE reform should be realistic about the existing political framework. Privatizing PetroChina and similar high-profile SOEs just does not seem conceivable in the current system (the privatizations of the late 1990s, under the “grasp the large, release the small” slogan, focused on locally-owned and nonstrategic firms).

In the paper I did a couple of years back on SOE reform, I was very careful not to aim for Washington Consensus-style idealized outcome, but to focus on what seemed plausible and possible in the Chinese context (and what I proposed had in fact been done before). So I consider myself to have pretty realistic expectations about what kind of SOE reform is plausible.

Yet even relative to modest expectations, reform has disappointed. It’s hard to overstate how depressed most China-watchers have become about the state of state-owned enterprise reform. After some promising signals in 2013 that seemed to indicate an openness to a new approach, it has just been one disappointment after another. Instead of more privatization and more professional management, there is instead a renewed love affair with forced mergers of large SOEs, a heightened emphasis on SOEs as instruments of government industrial policy, an increase in the Communist Party’s role in company management, and a proliferation of new “anticorruption” procedures to limit decision-making by SOE executives.

In a characteristically clear and concise post, Nick Lardy argues that the latest fashion for consolidation is a bad move:

These mega mergers may satisfy the ambition of the Chinese Communist Party to have more prominent national champions, but they aren’t likely to improve the efficiency of SOEs.

Barry Naughton, in one of his always-useful overviews of the policymaking process, similarly notes that:

There is a remarkable degree of consensus that [SOE reform] has, at a minimum, progressed too slowly and, at a maximum, failed altogether.

And the more I read from domestic commentators about the current SOE “reform” process, the more discouraged I get. Here are some excerpts from an interview with Yu Jing of CASS that give a flavor of the current conservative tone:

The basic idea of the previous round of [SOE] reform was to give full play to the role of the market, and accelerate integration with the more developed and more advanced global market system. Today, however, the international and domestic economic environment is not that optimistic, so a violent market reform could not only fail to achieve the goal of economic stability, but could even increase risk. …

The previous system for supervising state-owned enterprises had many regulations based on general principles; the current regulations have more attention to detail and focus on implementation. In the future, we still need to continually improve the system for supervising state-owned enterprises, and deal with the numerous problems that have been exposed. We need to have targeted constraints, and change the old method of after-the-fact supervision, so that the state-owned enterprise system can steadily improve. …

Future SOE reform will put greater emphasis on standards and norms, there will be more and more constraints on enterprises. For the top management of SOEs, they will face more difficult challenges in leading China’s large companies in a marketized and international direction, they will have to assume a more important historical responsibility. …

We should understand that the ultimate goal of SOE reform is–under the prerequisite of regularizing the operations and behavior of SOEs–to stimulate the vitality of SOEs, and to build a system that is more transparent, more standardized, and more in keeping with development of modern corporate culture.

The emphasis on avoiding risk is almost overwhelming. The “prerequisite” in the last sentence seems more important than the nod to “vitality”: SOE reform is not about making SOEs more like private-sector companies, but making them more like the government bureaucracy, where managers implement policy priorities while following detailed codes of conduct. This makes some sense if the priority is to avoid corruption at SOEs. And more checks and balances could reduce wasteful investment. But it does not seem like a recipe for raising the state sector’s extremely low return on capital.

The folks at the IMF, who have to come up with constructive suggestions rather than just complain, been reduced to suggesting that the government “pilot” serious SOE reform at one or two companies (implicitly making the point that the current approach is not going to solve the actual problems, so starting afresh is necessary). Here is Markus Rodlauer in a conference call after the IMF’s last Article IV report on China:

We have a view that it would be very helpful for China, both domestically and internationally to demonstrate a strong start to a new approach to state-owned enterprises. And the new approach, as we described it in the report, is comprehensive that addresses both the financing side of it, the debt side of it, the enterprise restructuring side of it, the social side of it, the employment consequences, altogether in a coherent way. And making a strong start with 1 or 2 or 3 large enterprises, to do it in the right way, then you also allow private investors, and even foreign investors to come in and play a role.

I think that’s a good suggestion, and I hope it gets traction, but it does seem like a sign of how far expectations for SOE reform have fallen.