There was an interesting presentation at the AEA meeting in Philadelphia from the team working on the World Wealth & Income Database that included a comparison of how privatization and inequality developed in Russia and China (link for AEA members).

The data work is quite impressive and useful; here for instance is a lovely chart showing the trajectories of privatization across China and Russia, with comparisons to the Czech Republic and the advanced economies:

This doesn’t change the usual understanding that Russia pursued a “big bang” or “shock therapy” approach to the privatization of state enterprises in the early 1990s, while China moved later and more gradually, but it does illustrate it very vividly (Czech appears to have pursued a strategy somewhat intermediate between the two).

Another noticeable trend in the data, which was not really discussed by the authors, is the flatlining of China’s public wealth share after around 2006. This fits nicely with my own observation that SOE reform and privatization came mostly to a halt in the period from 2003-06, partly in response to concerns about insiders illicitly enriching themselves off the privatization process. For instance, the phrase “preventing the loss of state assets” made its way into high-level policy documents for the first time in 2003, and is still being invoked today.

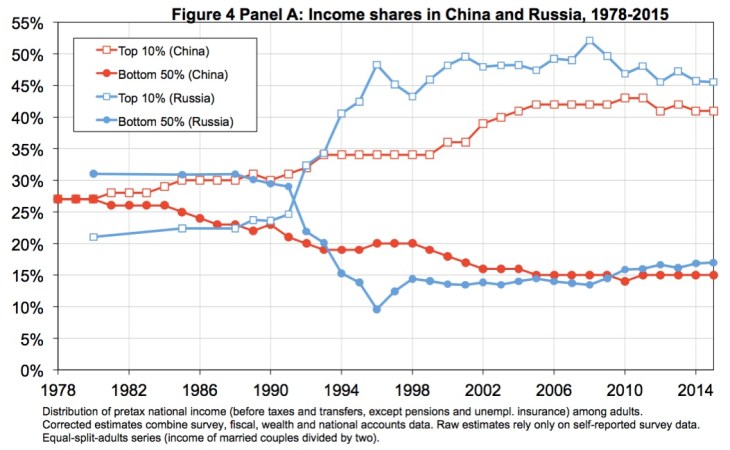

Why Chinese policymakers would want to avoid a Russia-style outcome is nicely captured in another chart on the evolution of inequality:

This data seems to make it pretty clear that the extreme increase in Russian inequality was indeed closely linked to the early 1990s privatization process, as has long been clear from more anecdotal and historical accounts. Other data presented by the authors (Filip Novokmet, Thomas Piketty, Li Yang, Gabriel Zucman) show that private wealth increased in Russia largely at the expense of public wealth–in other words, as a result of the transfer of assets–while in China private wealth increased more steadily as a result of rapid economic growth and housing reform.

I’ve been quite critical of China’s policies for state enterprises for a while now, since I think the lack of progress on privatization has allowed SOEs to become more inefficient and blocked the growth and market access of private firms. So this paper was a useful reminder that in the early 2000s China’s government had good reasons for wanting to be cautious about privatization.

The paper also suggests to me that Russia had two policy failures not just one: yes, privatization was mismanaged, but it also failed to drive broad economic growth in the aftermath of privatization. These two failures were obviously not unrelated but they are also analytically separable.

I don’t think that a resumption of SOE privatization in China would mean that broad-based economic growth would suffer; quite the reverse in fact. Measured inequality would probably increase as a result of more privatization, but I also doubt that current figures are really capturing the inequality produced by corruption and rent-extraction by SOE insiders.

There is more detail on all this in the original WID papers on Russia and China, which I haven’t yet gone through closely.