Harald Jähner’s recent book Aftermath: Life in the Fallout of the Third Reich 1945-55 is a fascinating window onto German life during the end of one social order and the creation of another one; it covers everything from “rubble tourism,” mass migration and regional cultures to to jazz dance halls, sex toys, interior decoration and avant-garde art.

There is also quite a lot on how the people living in Germany’s ruined cities made ends meet on a daily basis, through a combination of official rations, looting and the black market. Jähner’s reflections on how people’s lived experience of these different types of economic systems influenced their thinking is interesting if somewhat speculative:

In an atmosphere of mistrust and curiosity, the black market was a vital learning experience for the Germans, offering a radically different trading experience and providing a fundamental corrective to the Volk community fetishised by the Nazis. It was a lesson that remained in the memory for many years. Its lack of defined rules, which “rewarded the cunning and punished the weak,” created an economic terrain “in which people had apparently once more become wolves towards their fellows,” as the historian Malte Zierenberg writes. The widespread wariness so characteristic of the 1950s found a powerful source here. That narrow-minded, stuffy atmosphere that lingered around the black market was the smell of mistrust. Even the appetite for cleanliness, tidiness and order in 1950s Germany, which appeared strange to the next generation, had an origin in the chaotic conditions of the illegal markets.

The black market only thrived because of the existence of its opposite pole, the rationing system. On the one hand the wild interplay of raw market forces, on the other rationed per-capita distribution. People were caught between two different systems, always experiencing both at the same time: the state dirigisme of the shortage economy and the anarchic freedom of the unbridled market. Two conflicting logics of distribution, both of which had severe shortcomings.

This daily exercise in practical sociology, with all the exertions that it entailed, explains the unshakable faith that West Germans would later bring to the system of the “social market economy,” which, from 1948, became the patent remedy for the emerging Federal Republic. The very phrase sounded like a magical formula, because it reconciled both sides: the caring state ensuring that everybody got something and a free market system that was demand-led and placed the consumer at its centre. The few black-market years ensured that the social market economy became an article of faith for generations.

This “practical sociology” of ordinary people may not have directly determined the top-level government policy decisions that built Germany’s postwar social market economy. But the functioning of that system, like any other, depends on some shared consent to and understanding of economic norms.

His discussion also reminds me of the way popular support for the planned economy in China fell apart in the 1970s. At first this happened in the scattered local experiments with local agricultural markets and light industry that were facilitated by the chaos of the Cultural Revolution; Frank Dikotter’s wonderful 2016 article on “Decollectivization from Below” compiles a lot of fascinating archival material on this theme. The government’s later, more organized efforts to build a “socialist market economy” were informed by this widespread rejection of the old system, a discontent that was all the more effective because it was based on practical lived experience rather than ideological preconceptions (see my older post on China’s grassroots market liberals).

State capacity is a difficult concept to make concrete: a government’s ability to do stuff is obviously important, but how to tell if it is high or low? As a useful overview over at the Broadstreet blog shows, the most common way to measure state capacity in general is to measure fiscal capacity: the government’s ability to extract revenue from the economy. This makes sense historically, as the growth over the last few centuries of governments’ ability to do things like wage wars and provide social benefits went hand-in-hand with the development of tax systems and debt markets.

For the 20th century onward, the authors suggest a more precise metric: “To measure the fiscal capacity of the modern state, we use the share of income tax revenue in total tax revenue, as the collection of the income tax calls for high administrative capacity to ensure compliance.” This is an interesting choice, as on this measure China is a real edge case. Taking a quick look at the OECD Global Revenue Statistics Database, which covers over 100 nations, here is a list of the dozen countries with the lowest share of individual income tax revenue (for China only a 2019 figure is available, the others are the average of 2015-19):

Country

Individual income tax, share of tax revenue

Côte d’Ivoire

0.3%

Bolivia

0.8%

Paraguay

1.7%

Antigua and Barbuda

1.8%

Guatemala

3.4%

China

4.8%

Costa Rica

5.7%

Colombia

6.2%

Nicaragua

6.3%

Togo

7.0%

Cameroon

7.0%

Mali

7.3%

Source: OECD Global Revenue Statistics Database

A measure of state capacity on which China underperforms Nicaragua and Mali is probably a measure that is not capturing some important dimensions of actual state capacity. To take just some of the most obvious physical manifestations of administrative and technical ability, the governments of the other countries on this list are not operating their own rovers on Mars, or managing massive numbers of infrastructure construction projects both domestically and across borders. And whatever you think of China’s zero-Covid policies, it is unquestionable that local governments are displaying extraordinary logistical capabilities in organizing the mass testing of millions of people on short notice. The common claim that these policies demonstrate “China’s strong capacity for resource mobilization” is certainly correct (whether resources are being mobilized in the best way is another question).

Why does this measure get China wrong? To some extent, the focus on income taxes overly privileges a particular set of institutions as representing capacity. The actual structure of taxation reflects more than just administrative ability: which taxes are levied is a political decision. In recent decades, China’s government has consistently made the political decision to exempt most of the lower classes from income taxes, and to tolerate plenty of tax evasion by the upper classes.

It would indeed be difficult for China to build the administrative systems to levy a more broad-based income tax, but probably not impossible. China has, for instance, successfully administered a broad-based value-added tax for more than two decades. If you were to rank countries instead by the share of value-added taxes in total taxation, then China’s share of 30.2% would put it comfortably above the OECD average of 20.3% (and the US, of course, would be at the bottom with zero, as it has consistently made the political decision not to levy a VAT).

Nonetheless, there is still some useful information in the fact that China is an outlier in terms of this particular measure of state capacity. It suggests that the nature of China’s state capacity is different from that of your common or garden-variety Western social welfare state. The Chinese government’s ability to extract and mobilize resources does not work primarily through formal fiscal channels. It is well known that off-budget instruments like local-government land sales and the operations of state-owned enterprises are extremely important in the economy.

More broadly, both the strengths and the weaknesses of the Chinese state are tied up with its peculiar institutional structure and political heritage. China is a Leninist party-state that penetrates the private sector and civil society, operates more through political directives than formal legal instruments, and regularly undertakes mobilizational campaigns to achieve society-wide transformation. The capacity of its Leninist institutions is hard to measure precisely because they often hide behind conventional state forms, but is no less real for that.

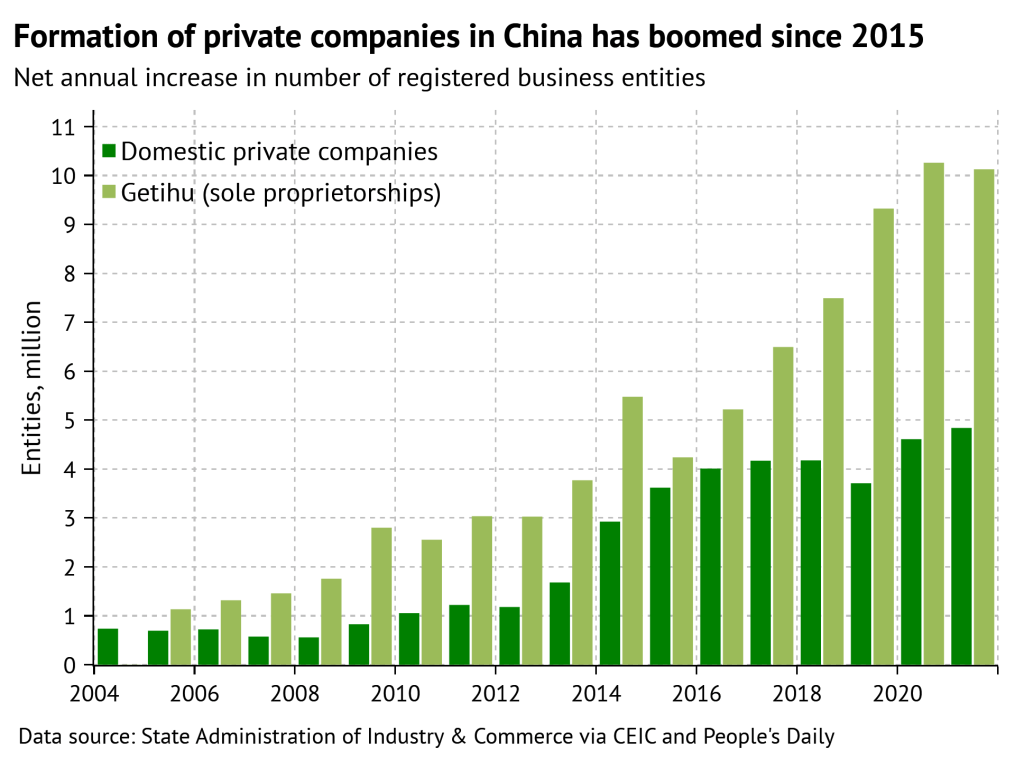

Here is an interesting empirical fact about the Chinese economy that does not easily fit into the usual narratives: under Xi Jinping, more new private-sector companies are being created every year than at any period in its modern history. This of course is exactly the kind of factoid China’s government regularly trots out to demonstrate the vitality of its private sector. In March, the People’s Daily published a front-page article extolling the fact that the number of private companies had quadrupled from 10.9 million in 2012, when Xi took office, to 44.6 million in 2021. (I don’t actually read the People’s Daily every day, but I do subscribe to Manoj Kewalramani’s invaluable Tracking People’s Daily newsletter). Company formation is one of the ways of tracking what is usually called business dynamism: how much entrepreneurial activity is happening in an economy.

The figures are even more interesting than the propagandists seemed to realize. While the official publication of company registration data has been intermittent at best, the People’s Dailyarticle and accompanying chart allow some of the holes in that published data to be filled in. The combined data provide a picture of private-company formation in China over roughly the past two decades. Before 2012, the population of private local companies was increasing by around 1 million or less every year (this is the net increase; there is even less data available on the gross number of new company registrations). Net company formation accelerated over 2013-15, and since 2016 has been running steadily around 4 million or more per year. There’s been an even more dramatic acceleration in the formation of new sole proprietorships (getihu: not companies with a separate legal existence, but businesses run as part of a household): the net increase was over 10 million in both 2020 and 2021, up from around 3 million in 2021.

That is a pretty dramatic change in the trend. The cause is well-documented: a systematic official effort, beginning around 2014 and continuing through the present day, to lower the costs and simplify the process of forming new companies (I wrote a piece about it back in 2014). The OECD is one of the few organizations that have attempted to systematically evaluate the effects of these changes (the much-maligned Doing Business survey of the World Bank was another). Here is some commentary from its just-published 2022 Economic Survey of China, which quantifies the administrative burdens on start-ups relative to other countries:

Enterprises in China are subject to somewhat lighter burden than in the average OECD country, though higher than in Japan, Germany or Italy. In some major non-OECD economies, such as Brazil or South Africa, the burden is much higher than in China. … Only one institution needs to be contacted to start a business in China, compared with the OECD average of around four. This is the same as in the frontrunner countries of Australia, Canada, Greece, Korea, Latvia, Lithuania or New Zealand, where to set up a new firm it is also enough to contact a single institution. There is neither minimum capital requirement nor monetary costs for registering a limited liability firm in China, which is in line with the best practice in OECD countries.

Substantially reducing the barriers to company formation to close to rich-country levels is a pretty decent accomplishment. It’s not a bad legacy for Premier Li Keqiang, whose signature initiative this has been and who is finishing his last year in office. What’s curious, though, is that the enormous boom in private-company formation in recent years has not had very visible macroeconomic effects. Economic growth is not any faster: growth in labor productivity has averaged 6.6% annually in the seven years since 2015, compared to 8.4% in the prior seven years. Of course, a lot of factors have combined to slow China’s economic growth recently, so growth might have slowed even more without this boom in company formation.

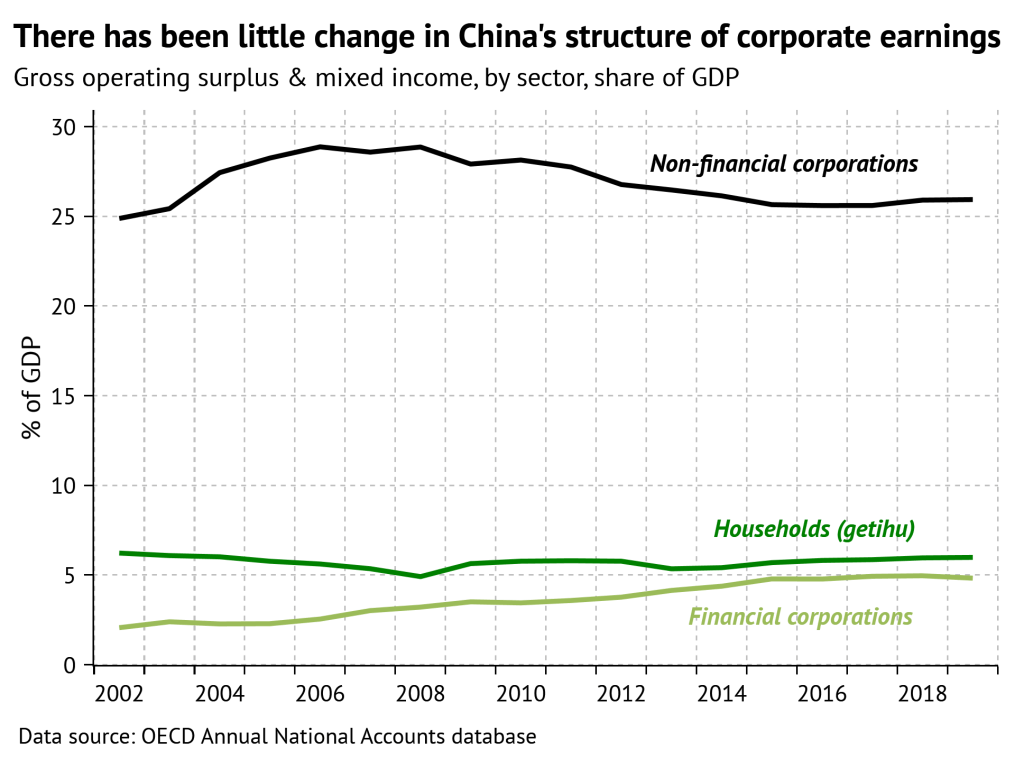

But there also hasn’t been any noticeable change in the structure of national income. Since barriers to company formation have fallen, and the pace of company formation has increased, we might reasonably think that a greater share of economic activity is now taking place inside legal corporate entities rather than in the informal economy. Yet the share of corporate profits in national income (technically, gross operating surplus in the fund of flows) has remained basically unchanged around 26% since 2015. Business profits generated by households rather than companies (through sole proprietorships, getihu), have also been stable around 5% of GDP. (The chart below uses the OECD’s presentation of China’s flow of funds, which is more standardized and easier to interpret than the one published by the National Bureau of Statistics; thanks to Bert Hofman for the pointer).

In other words, although the population of private companies in China has gotten much larger, the share of economic activity generated by those companies has not. Some of the increase in private company formation could thus be because it is now easier for people to create multiple corporate legal entities, rather than because there has been a true increase in the rate of entrepreneurship.

The flow of funds data goes only to 2019, and so doesn’t show what happened during the two pandemic years of 2020 and 2021. By all accounts, these were horrible periods for small businesses in consumer-facing services like restaurants and tourism. They lost huge revenues during the initial lockdown of 2020, enjoyed a few months of rebound in the latter half of 2020, and then settled in for months of disappointment in 2021 as waves of intermittent Covid restrictions discouraged travel and recreation. Things have obviously gotten even worse in 2022. Data from OECD countries show that new firm creation generally fell substantially in 2020, so the fact that in China net company formation actually picked up is surprising. Of course, China’s pandemic economic trajectory in 2020 was quite different from the OECD countries. But it’s also possible that the well-documented mass closures of small business during lockdowns are not fully showing up in the company registration data: companies could stop operating without canceling their registration. (Friends who have companies in China tell me that canceling your registration is difficult and time-consuming and often not worth the bother.)

The biggest surge in registrations has not been for private companies but for sole proprietors/getihu: the pace in 2020-21 was roughly double that of 2015-16. Because sole proprietorships have inherent limitations to scale (they can’t hire more than a few people) and no limited liability, they are usually more of a vehicle for self-employment. The desire to be an entrepreneur can be a reason to choose self-employment, but in developing countries like China, self-employment is often the result of a lack of more stable job opportunities. It can also be the channel for more modern forms of unstable employment: drivers for delivery and ride-hailing services often register as sole proprietors, which makes them contractors not employees. The increase in sole proprietorships does appear to be part of a broader structural change in China’s employment patterns: an important 2020 article by Scott Rozelle and colleagues documents a sustained rise in the share of employment in informal, low-wage service sectors.

It’s certainly not a bad thing that it has become easier for Chinese people to establish companies. But the rather ambiguous economic evidence suggests that the surge in private-company formation over the last several years is not a simple story of rising business dynamism.