In Beijing earlier this month, I bumped into some former colleagues from the foreign press corps, and was invited to come talk to the Foreign Correspondents’ Club of China. As a former officer of the FCCC, I could not turn down such an invitation. Below is a transcript of that session on May 3; it was all Q&A, pretty lively, and we covered a lot of ground. I’ve cut out a few bits where my answers were short or unilluminating, and smoothed out the speech for easier reading.

· · ·

Q: Andrew, maybe we start with this. I saw you wrote a piece the other day about the Politburo on the state of the economy last week and which I also found very interesting. So what are the other key takeaways from this meeting? The signals seem to be more mixed, not really upbeat, enthusiastic but more sober as far as I understand.

A: I think there are a few key messages from the Politburo meeting.

The first was basically to deliver a positive assessment of the economy: they said very clearly that the economy is performing better than expected. I guess it depends whose expectations that is relative to, and I think they mean their own expectations as of late last year. If we think back a bit, remember that a lot of people worried that there would be multiple waves of Covid outbreaks and that the economy wouldn’t really get going until Q2. And in fact Covid wrapped up pretty quickly and things started to get back to normal just before Chinese New Year. So overall, the first quarter was better than expected for that reason.

The corollary to the better than expected outcome is that they don’t need to necessarily juice the economy a lot more. The economic policies that they’ve taken over the past year have been pretty extensive, but I think a lot of them didn’t really have a chance to work cause of the disruption from Covid lockdowns. There’s a cumulative effect of various things they’ve done in terms of loosening property market policies, cutting interest rates, expanding credit growth. Basically all of that stuff is hitting the economy now as a delayed impact over several months. I think their assessment is that this stuff is working, it’s feeding its way through into the economy, and we don’t necessarily need to pump it up a lot more since growth has already accelerated.

And then another key message was really to reassure people that the disruptions of the last couple of years will not return. So you’ve seen in the rhetoric very clearly over the last few months this repeated mention of support for the private sector, even specifically support for the internet platform companies that were the target of severe regulatory action in 2021. That’s a pretty clear shift in the signaling on this particular issue.

There is a longer term question that everybody acknowledges, and I think it’s interesting that the Politburo also acknowledged it in the communique. Yes, we’re having this bounce back in consumption. Everybody can see that, it’s a natural process. Obviously people have been prevented from consuming as normal for quite some time. So we should expect that they come back and do some of the things that they’ve been wanting to do for a long time. But is that really enough to drive sustainable growth for the economy over more than the very short term?

Q: What we’ve seen over the past few weeks is more like an overshooting of consumption as people want to travel again. Over the next few weeks, we might see a moderation, and see that this was more or less revenge spending and then things will normalize. I’m thinking of unemployment rates among the youth, and I’m thinking of lagging household income growth. And then at the same time we’ve seen private investments are still pretty low. So that this ends up like an L-shaped recovery, which will then moderate very fast during the second half of the year probably.

A: Yeah, that’s one view. My view is a little bit different, and is maybe a little more optimistic than that. I don’t think consumption is overshooting right now. If we look at different indicators of consumer spending, they’re still below where they should be based on the pre-pandemic trends. Right? If we just assume that those growth rates had continued, then household spending should be up here, and instead it’s still about here.

So, I don’t think that consumption is overshooting. I think it’s in the process of getting back to trend. And there’s still more room for consumption to continue to improve in coming months. In the very short term, there is this kind of snapback dynamic. There’s probably a lot of pent-up demand in the first quarter, and maybe some of that comes off a bit in April. But early indications are that the travel for the May Day holiday was also pretty good. So maybe things pick up again in May. I’m not the expert on this kind of micro forecasting of what the Chinese economy is doing week by week. But my basic view is that the rebound in consumption has started and it still has some way to run rather than already being exhausted.

And I think the prospects for the second half of the year are actually a little bit better. One reason is that in this initial phase of reopening from Covid, you’re seeing what I would call trickle-down consumption.

You have the high-income households, the people who were able to wait out the lockdowns working on their laptops from home, whose salaries were not cut, who didn’t lose their jobs. They have household savings, and they have the same income that they had before Covid, or even higher, and just haven’t been able to consume as normal. They have come out in force in the initial stages. And as they spend more on recreation, services, travel, all that stuff, they support employment in service sectors and create more jobs. Then you’ll see some of those gains trickle down to lower parts of the household income distribution.

So I think in the first half of the year you have this initial boom of spending from the upper half of the distribution. We’re already seeing signs that the the job market is improving, unemployment is coming down. Business surveys show that companies are hiring more and worth paying higher wages. This stuff takes effect with a little bit of a lag, and I think it will show up more obviously in the second half of the year.

· · ·

Q: One interesting thing that was in the readout from the Politburo meeting, and you also mentioned it during your first answer, that there’s a commitment that they’re not going to repeat the mistakes of the past, like on internet platforms and private business and so on. How can we be really sure that this is not going to happen? I mean, we’ve just seen very loud commitments to foreign investment and they want foreign companies to come in. At the same time they’re raiding the offices of foreign companies. And so there’s always, in my view at least, a gap between the official rhetoric and then what’s going to happen on the ground and in the provinces and cities.

A: Yeah, that’s obviously a very fair point. I think generally there’s an issue with authoritarian regimes making promises about what actions they will take in the future. Because by the nature of the regime, their actions are not bound by any external constraint. So it’s hard for them to credibly commit to not doing certain things. They may feel like not doing them now, but if they feel like doing them later, there’s nothing to stop them basically.

I guess my view on this is a little bit cynical. There’s a school of thought out there that that the new administration led by the new Premier is trying to bring back a quote unquote pragmatic, quote unquote business-friendly, style of policy making. I think that’s true in kind of a short-term tactical sense. I don’t think it’s true in a long-term strategic sense.

The the top guy has been pretty clear that he wants to reorient the way the Chinese bureaucracy functions away from the all-out pursuit of economic growth and towards the pursuit of a different set of goals. And I think the style of policy making that people now conventionally describe as pragmatic and business-friendly was really an artifact of that previous policy orientation — where every government official at every level knew that they had to do anything they could to support economic growth. And that’s not the regime that we’re currently in.

· · ·

Q: Can the youth unemployment problem be solved in coming years? Or is it some kind of structural problem? There’s more and more young people coming to the job work market from the universities every year.

A: I think high youth unemployment right now is a cyclical problem, not a structural problem. I think it’s a result of basically everything that happened during Covid with all the lockdowns that destroyed a lot of service sector employment, which is precisely the kind of jobs that young people tend to take at the very early stage of their career.

Right now I think that youth unemployment is just kind of a more volatile indicator of overall unemployment. It’s higher than total unemployment. But as total unemployment comes down, I think youth unemployment should also come down. That’s based on the argument that I just made, that the improved consumer spending on services is going to create jobs, or restore jobs that were destroyed over the last three years, since there is some recent improvement there.

I think there is a structural mismatch in the Chinese labor market. I’m not sure if high youth unemployment is exactly the right diagnosis for it. Basically you’ve had a huge expansion of university education over the last couple of decades. So right now the system is producing a lot of people who, because they have university degrees, want to be white collar employees. And that is the whole point of having a university degree: that you can be a white-collar salaried employee and work with your mind and not with your hands. But in fact, a lot of the jobs that the economy is creating are more blue-collar jobs where you do work with your hands and not with your mind.

So I think there is a kind of a structural mismatch. I’m not sure there’s a mismatch in terms of the number of people, but there is a mismatch in terms of people’s expectations about what kind of jobs that they’re entitled to as a result of their own efforts, and then what kind of jobs the economy is actually offering.

· · ·

Q: Can I just go back to what you were saying about the overall policy direction and to ask you what do you think foreign investors ought to think about common prosperity, what it means for them? You can also tell us what you think it means.

A: One interpretation of the rhetoric on common prosperity is that the government wishes to have a more explicitly left-wing, socialist, social democratic, call it what you will, type of policy and be more aggressive in redistributing incomes. Some people are worried about that because they see a lot of China’s success as having come from pursuing relatively more liberal, free-market policies rather than these kinds of measures that we’d associate with European social welfare states.

I don’t think that’s what common prosperity actually is. So if people are worried that there is going to be new government program to expand the welfare state and redistribute income, they can rest assured that, at least in my view, that’s not going to happen.

I think the common prosperity rhetoric is more political signaling from the top. It’s more a kind of political campaign to signal the administration’s adherence to socialist values.

It is, strangely enough, not really connected to specific policy discussions. In fact, if you read the debates about common prosperity domestically, there’s a lot of people who are saying, well, we have this goal of common prosperity, that means we should implement measures like, better unemployment insurance, or a better pension system. And yet there doesn’t seem to be any actual interest in or movement toward doing these things.

So I don’t think the common prosperity rhetoric is a sign of a so-called leftist tilt in Chinese policymaking. The actual substance of it is a bit harder to interpret, I think, for outsiders. But again it is, in my view, more of a political campaign that’s oriented around symbolic gestures rather than substantive changes in economic policy.

· · ·

Q: What’s going on in the property market?

A: Property, always a super interesting question for China. I think the surprise in the first couple months of this year is that property market sentiment was actually pretty decent. Sales were up quite a lot, and prices are rising in most of the cities. Again, I think there’s this pent-up demand issue where a lot of stuff snaps back immediately after the reopening. Maybe it doesn’t last quite as long, and property sales have tailed off a bit from where they were in January and February. But they’re still running decently above last year’s level.

So it does seem that in fact property is going to be a growth contributor for China this year, which is not something that a lot of people necessarily expected last year when we went through the biggest property market correction in modern Chinese history.

The outlook past this year I think is a little more equivocal. It’s our view and the view I think of pretty much everyone that the fundamental demand for housing in China is probably at or past its peak. It’s probably not a growth sector for the economy in the future. So it’s going to be stable or declining as a share of the economy, which means it’s going to be be subtracting from growth rather than adding to it, on average, in the future.

This year sales are likely to be okay. Construction is not that great. But if sales have a good year, and property developers’ financial situation improves, they’ll leave it more cashed up. So you can maybe have decent construction into next year as well.

But again, I think these are short-term cyclical dynamics. If you look at the government’s signaling on property policy, it’s pretty consistent. Of course they realize that last year was kind of a mess, and they want to get out of that mess, and get the market back to more normal levels of activity.

But they’ve been engaged in an effort over the last several years to actively try to wean the economy of its reliance on real estate, and to bring down levels of leverage of property developers and generally shift the balance of the sector away from private-sector profit maximization and towards more fulfilling a public-service role where there’s more construction of social housing, rental housing and other stuff that’s not as purely profitable as the private luxury market stuff. So I think the direction of travel for the property sector is pretty clear by now.

Q: What can China do in terms of finding new growth sectors for the economy to replace property and real estate? And then the second question is what could China do to prepare its economy for the possibility of conflict over Taiwan?

A: These are both great questions. And in fact, they’re the same question, at least I think from the perspective of the government. So what I thought was the most interesting about the both the Politburo meeting that we just had, and also a lot of the other rhetoric that’s been coming out of the government, is that after the Party Congress, the leadership seems intent on reorienting government priorities towards this geopolitical competition with the US.

And the overriding economic priority is to build up the economy so that it can survive, prosper and prevail in that competition. Of course that means increasing scientific and technological self-reliance, which they have talked about ad nauseum for several years now. And we’re also now seeing this language about building a modernized industrial system, and this seems to have some security connotations.

What I think is going on is that the government essentially wants to drive growth by investing in a whole-of-society effort to reshape the Chinese economy for this geopolitical competition with the US. They think that not only is this a national security priority, but it is also something that can be a growth driver for the economy.

The first of those is something that we’ve known already over the last couple years. And what I think is interesting is that they gave this indication that they see this refashioning of China’s industrial base not just as a security issue, but also as the core of their economic policy.

Q: A related question is do you feel also that the economy is changing more into a war economy? Especially if you look at what’s happening at the countryside, more stress on producing, let’s say rice and less on producing tea, et cetera.

A: I don’t think I would describe it as a war economy. But what we do see is a generalized focus on national security, what they call the holistic national security concept which encompasses many different areas including food security, which is obviously a very close interest of Xi’s, energy security, technological security, and so on and so forth.

I think it’s a general effort to harden the economy against external shocks. I wouldn’t go so far as to say it’s an effort to put the economy on a war footing. I don’t see evidence of that. But it is based on the recognition that China is operating in what they view as a more uncertain, more hostile world. It’s their responsibility to protect the economy from external forces.

· · ·

Q: China has a 17% value added tax. So if you reduce the value added tax, would that help increase consumption?

A: I’m going to kind of dodge the question and say I don’t think they’re going to do that. The reason is that China actually has very few reliable sources of tax revenue. Their tax structure is quite unusual. It’s heavily reliant on the VAT, the corporate income tax and then various transaction taxes including taxes on property and other stuff like that.

If you look at the government revenue structures of the US and European countries, they get a lot of revenue from the individual income tax, and that’s basically what they use to fund welfare states. China has made a political decision of long standing that they’re not going to have substantial direct taxation of household incomes.

And so that creates some constraints for them in terms of what they can do with government revenue. They’ve already cut corporate taxes substantially over the last several years. I can’t remember the figures off the top of my head, but the taxation of companies as a share of GDP has gone down substantially since 2016.

And they have, as you know, a lot of future obligations. They’ve got this burden of the aging population to deal with. They’ve got this massive local government debt problem, which the central government is probably going to have to use its own financial resources to solve.

Basically in the future they need more tax revenue, not less. So I think it’s pretty unlikely that they would substantially cut the VAT because it’s their best source of tax revenue.

· · ·

Q: Just a short question on the GDP growth target. Do you think they’re ever going to get rid of it?

A: I think this is an interesting question. One of the things that Xi Jinping did at the Party Congress in 2017 was to signal a shift away from the focus on GDP growth as the be-all and end-all of China’s political objectives. And so it’s kind of interesting that, in that context, they still retain a GDP growth target. Even though the political messaging around the target and the administrative structure around it is quite different.

People have different theories about this. One of the theories is just that there’s a lot of inertia in the Chinese system and actually a lot of different departments in the Chinese government need the GDP target as a kind of a reference. They need to have some kind of number to base their plans for the coming year on. If they don’t have a GDP target then what number are they going to use? You need some kind of anchor for just the internal forecasting and budgeting work of the government. Since you have to have some target, since there has to be some kind of internal reference, you might as well keep it.

There’s also been for been for many years, as you know, a view that having the GDP target was distorting, that it created incentives for local governments in particular to act in destructive ways. I actually remember many times when I was on the other side of the microphone and calling up various economists to ask them for quotes, and they would always say, oh, you know, China has to get rid the GDP target and transition to a market-based economy and blah, blah, blah.

I think actually the GDP targets serve as a useful discipline on the government. They are to some extent a remnant of the previous regime in which government policy was oriented around the pursuit of economic growth, and the need to ensure economic growth acted as kind of a disciplining mechanism on government decisions. So if they knew that doing X would have a large negative impact on economic growth, that was a good reason for not doing X. And then if you don’t have a GDP growth target and you don’t have the necessity to drive growth so much, then you might go ahead and do X anyway, and that wouldn’t be good.

So I think in the Chinese political system, the GDP growth targets do serve a useful function in terms of putting some guardrails around the government’s intervention in the economy. My view, maybe it’s a bit against consensus, is that keeping them for the moment is actually not a bad thing.

· · ·

Q: If I understand right, you said earlier that the government in China wants to drive the growth by investing in preparing the society and economy for political competition with United States, self-reliance on food, energy, science, technology, et cetera. If suddenly they are putting a whole lot of energy and resources into making themselves self-reliant rather than focusing on making money and getting foreign factories in, isn’t it going to be more costs than profit? It’s going to be a huge gamble right now. So the question is does the Chinese focus on increasing self-reliance and economic security impose a cost on the economy, relative to a more open trajectory?

A: The standard economist’s answer to this would be absolutely yes. The reason that you have this globally distributed division of labor in the semiconductor industry and many other sectors is that you have a high degree of specialization in different functions across different geographies. By arranging things in this way, everyone can do what they’re best at, and then the overall profitability and efficiency of the system is maximized.

So what China is doing in terms of trying to replicate domestically capabilities which already exist outside of China is in a sense duplicative investment. Is it really going to benefit the economy to invest in doing these things which don’t really push the frontier of human knowledge forward, but just kind of repeat and duplicate what already exists? Probably that is a lower productivity trajectory for Chinese investment.

But as you know, the reason that they are doing this is that they see even greater risks that they would be denied access to these critical inputs, to critical materials and the ability to build up their technological base. So it is worth spending some money to avert that risk in the future. I think that’s ultimately a political judgment rather than an economic judgment. The reasons why they are doing that are pretty clear. And they are not imaginary, these are real issues for them.

· · ·

Q: I was wondering could you say something about the impact of de-risking from China, which we are hearing about all the time, not just in tech but in many sectors. I think last year, a quarter of European companies said they were considering shifting their investments, but considering and doing as of course, a different thing. As far as you can tell, is it happening on a big scale, does it have an impact on the overall economy?

A: This is a tricky one. The data on this stuff are hard to read to be honest. The IMF had a study in the most recent World Economic Outlook report which looked at FDI data and found some evidence that there was a shift at the margin away from China as a destination for investment. That’s probably the best look at the underlying realities that I’m aware of right now.

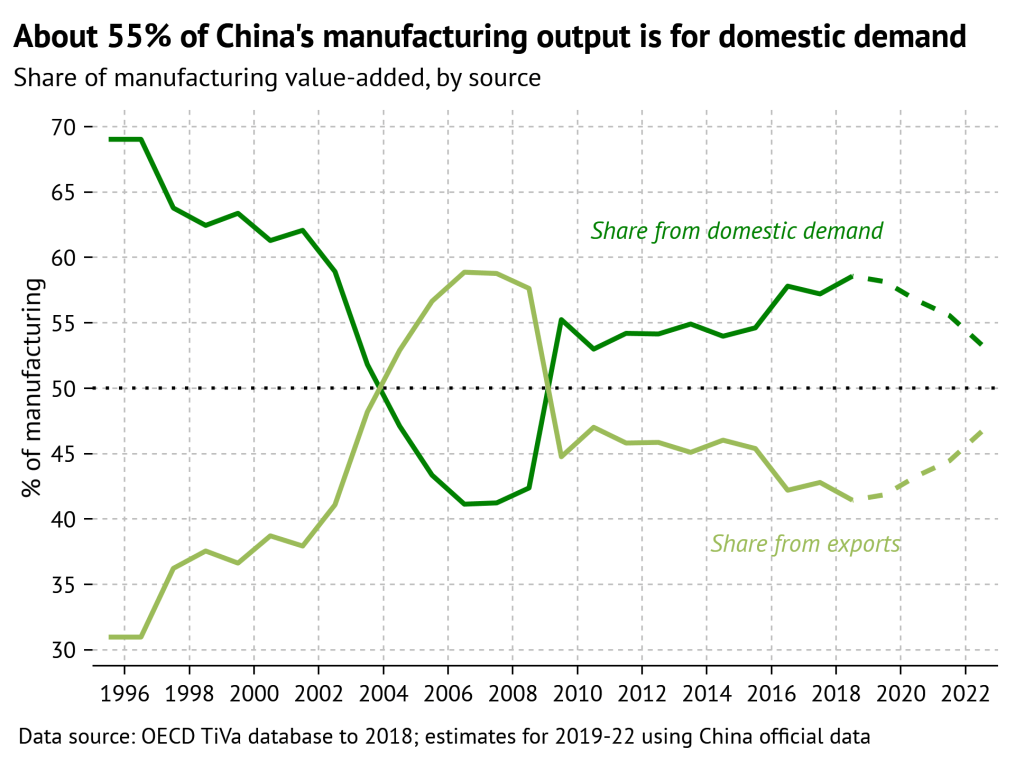

I would say, based on my conversations with foreign businesses and what I’ve seen here that there is a general shift away from using China as a global export base and more towards being in China to serve the Chinese market.

Multinationals have always had multiple strategies relative to China. Obviously China is the world’s second-largest economy, it’s not going away. If you want to be a globally successful producer of consumer or producer goods you need to have a presence in the Chinese market. So for many companies that hasn’t changed, nor can it change in a reasonable way.

But there’s been another aspect of that, which is using China as a manufacturing base to supply markets outside of China. The trade war with the US, various supply chain disruptions, the general perception of higher geopolitical risk due to the bad state of US-China relations, I think all of that all can change people’s thinking on this.

There’s a shift at the margin here. None of this stuff happens very rapidly. Factories take a long time to build. So this is a multi-year process process. And I don’t think you’re going to see dramatic exits from China. But I do think there has been a real shift in people’s understanding of the balance of risks relative to China that’s going to affect their presence here.

· · ·

Q: You mentioned that you’ve been noticing that national security has been driving the leadership. Is there a coherent model that the government has in mind of a a national security focused economic strategy?

A: Hmm, I’m going to say no. But there’s a grand Chinese tradition of figuring things out as you go along, right? Crossing the river by feeling the stones. So I think they know the direction that they would like to go in. And so they will try to figure things out as they head in that direction.

Again going back to the Politburo meeting last week and the readout from that, one of the interesting things is that they they highlighted the success of China’s electric vehicle industry. What is now getting global notice is the EV exports surge, particularly into Europe. And also you’re seeing the domestic EV brands really take over the domestic market and the legacy foreign automakers are quite worried about their prospects here. So I think it’s reasonable that China sees that as a success for industrial policy. They moved ahead with investing in a a new economic sector, and attained a leadership position that they can now leverage to support the overall economy.

I’m not sure that the EV industry is a model that’s easily replicable. Generational transitions in the single most important durable consumer good don’t come along very often. So there’s not necessarily another consumer product that’s comparable to cars that’s going to go through a comparable technological transition out there.

Also, and I think this goes back to the question about de-risking, one of the reasons you’ve seen the success of the EV industry and particularly of EV exports is that China was chosen as a global manufacturing base by global producers, most notably Tesla but also some of the other European brands. So the EV exports from China are not all Chinese brands, there are foreign brands in there. And that reflects decisions about supply chains that were made many years in advance because it takes a long time to build factories and put together the whole industrial chain.

I think, given the current geopolitical situation in the world, that it’s hard to envisage multinational companies deciding to make China the global export base for whatever their next big product is. Maybe that decision was understandable five or six years ago. I think it would be a lot harder to make that kind of decision now.

So the particular model that China followed in EVs, which was heavily domestically focused but also relied on this global manufacturing base, I think will be harder to do again in the future.

Q: I was quite struck when you characterized the potential growth drivers in China around self-reliance and national security. You go back a couple years to the five-year plan, there was really a strong theme about investments in basic research, science and technology. And obviously that can work pretty well with the way that you characterized the potential growth drivers in China.

Another way of characterizing that is a movement up the value chain into higher value manufacturing, higher value jobs. There was, at that time, almost a sense that policy makers saw this industrial change as a bit of a silver bullet for some of the economic woes: Invest more in high value industry to transform China from low value manufacturing to high value manufacturing, high paying jobs.

Now, I think you’ve sort of touched on the fact that there isn’t a coherent model yet, or there’s a variety of models. There’s the EV model and the chip model and the aircraft manufacturing model. They’re all pretty different. I guess I was wondering, what do you think China’s prospects are for moving up the value chain longer term, noting the challenges you’ve laid out?

A: So is moving up the value chain a focus of policymakers? Absolutely. But I think one thing that’s implied by the more intense focus on national security that we see now relative to even a few years ago is that it’s not just about moving up the value chain. It’s about keeping the entirety of the value chain within China, or at least, under effective control by China.

So I think there’s a slightly different conception here. Yes, China wants to occupy the high end so that they can compete effectively at a global level with the advanced economies. But also, I don’t think that they’re as relaxed maybe as they would’ve been in a previous generation about seeing some of that low end stuff go away. Maybe they’re going to feel that there’s a more of a need to keep those kind of basic components within China security and controllability purposes.

Moving up the value chain, this kind of rhetoric, is based on the theory of globalization, where you have have this geographic specialization at different points in the supply chain. So as one country moves to the high end of the supply chain, another country can come in and occupy you the medium and lower ends. And then you have high levels of global trade to make the whole thing work.

If, as both US and Chinese leaders have seemed to signal recently, we are moving into an era where countries don’t take globalization for granted, they don’t take high levels of trade for granted and they see a higher necessity of controlling for risks and uncertainty, then it implies a kind of a different orientation towards the position in the value chain. And not necessarily to vacate positions in the value chain as they move up.