After many years of working on China, I can still be surprised by just how big it is. It’s simple to say “China is huge,” but harder to really think through what it means. Nonetheless, a lot of people seem to think that size does not matter in any fundamental sense–the example I have in mind is the gent who years ago told me that “China is just Japan 20 years later and 10 times bigger,” which in fact is a surprisingly powerful rule of thumb. But I have to say that I suspect that some things do work differently in China because of its size, and that this is not well understood because we have no comparable examples to work with. We might call this the view, sometimes attributed to Stalin, that “quantity has a quality all its own.”

This question came to mind again after I read some interesting comments in a recent paper by the excellent Carsten Holz, the world’s foremost expert on Chinese statistics as well as a generally very thoughtful guy. The paper is not mostly about this question of size but he discusses it in passing:

China’s size is a new phenomenon in the study of developing economies. South Korea tried to develop a broad industrial base but soon began to specialize. Taiwan quickly abandoned plans for broad-based economic growth and focused on developing areas of comparative advantage, in many instances serving niche markets around the world. However, for China there are as yet no signs of significant specialization.

Across virtually all industries in China, the optimal firm size—the firm size with lowest per-unit production costs—is below market demand. I.e., there is sufficient market demand in every sector of the economy for several firms to co-exist and compete. The prospect of historically unprecedented domestic market size may yet lead to innovations in optimal firm size at lower per-unit production costs than hitherto experienced around the world.

Viewed from an international perspective, focusing on comparative advantage makes little sense for China: world demand may simply not be big enough to support any substantial degree of specialization in China. For example, for some electronics products China may already be the dominant world supplier, without, however, the electronics manufacturing industry dominating the Chinese manufacturing sector. In this case, world demand has driven specialization in production by China, except that in the Chinese economy the resulting degree of specialization is barely noticeable. As a result, one can expect to see ongoing investment across virtually every sector of the Chinese economy.

I found this a very striking idea, as one of the (many) things about China’s economy that has puzzled me in recent years is the apparent lack of specialization in its exports. There was fairly dramatic structural change in China’s exports up until about 2007, but since then the export structure has been largely stable. Exports have been growing, and China’s global market share has been rising until very recently. So China has generally been steadily becoming a more successful exporter. But as this has happened it has not shown much sign of becoming more specialized in particular types of products, which is usually one of the things that happens in countries that are successful exporters.

I had speculated that global demand was a limiting factor here: in the aftermath of the financial crisis, global demand for the kinds of things that China wants to specialize in–capital goods and equipment–has probably not expanded rapidly enough for China to have exported a lot more of those goods. But perhaps, as Carsten suggests, the issue is more fundamental, and one we have not really encountered before: China’s export industries might already large enough, relative to total world demand, that even a very successful export performance will not show up as much specialization. This is one to ponder further.

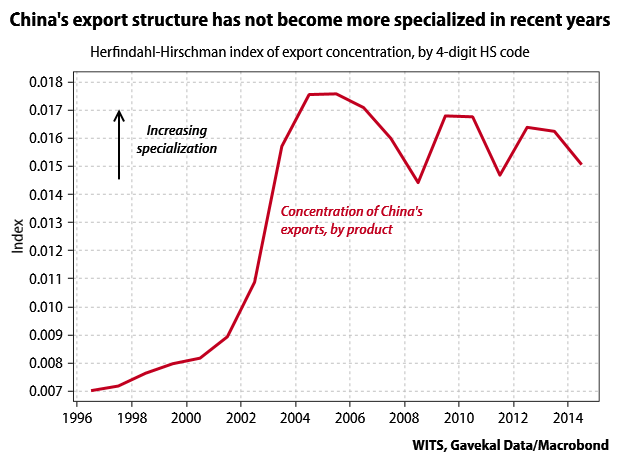

Update. Here is a more precise measure of export specialization — a simple Herfindahl-Hirschman index of concentration, calculated at the 4-digit HS level (it’s the sum of the squares of the share of each product in the total). This actually shows export concentration has been bouncing around in a range since around 2003-04, so it looks less like a cyclical post-crisis phenomenon.

The lack of China’s specialization in exports is possibly due to government decree, see this Reuters article on China import restrictions for Chinese firms: http://www.firstpost.com/fwire/amid-global-price-rout-china-crude-oil-imports-hit-record-reuters-2583134.html (Wu Kang, Beijing-based vice chairman of FGE Asia, said the two driving factors behind growth in 2015 were new demand from small, independent “teapot” refineries who gained the right to use imported crude oil in the latter part of the year, and stockbuilding in strategic reserves and commercial storage.)

Firstly, China’s Economic Complexity Index has skyrocketed since 2008. The broader categories may not show much change, but the narrower ones do.

“But as this has happened it has not shown much sign of becoming more specialized in particular types of products, which is usually one of the things that happens in countries that are successful exporters.”

-??? Any evidence for this claim? Diversity of exports is strongly correlated with the export of non-ubiquitous goods. However, diversity of exports peaks at around Uruguay or Belarus’s level of per capita GDP, while the export of non-ubiquitous goods continues to rise as old economy industries disappear.

I get a taste of China’s size every time I visit. Last month, in Kunming, I visited what I thought was the tea market: several blocks of buildings housing tea merchants and associated services. It was huge, looked prosperous and was very busy. Then my local friend told me that it is one of seven such tea markets in the city, some of which are larger.

I tend to think that “China” is the wrong unit for thinking about almost anything. I know we have to, because it’s a nation state, but casual reference to some notional “China” is much too prevalent. No-one takes seriously arguments about an undifferentiated “Europe”, though that continent may be pretty much as much of a unit as China.

Your blog raises intriguing questions. Here are three of them

Q1: Does this imply that data collected on excess capacity may have to be re-considered?

Q2: As China is a big player (if not the biggest) in global markets for quite a number of manufacturing industries, is it fair to assume that China may act as a price setter ( which, if true, would be quite unique among emerging and developing countries)? Or are global brand leaders and EMS providers retaining their capacity as price setters?

Q3: As “some things work differently in China because of its size, what would this imply for Dani Rodrik’s concept of “premature deindustrialization”? [Most developing countries tend to be small in global markets for manufacturing, and hence act as price takers. “As price takers, however, these developing countries may have “imported” deindustrialization from the abroad.” (Rodrik, 2015: 22).

Thanks for the questions Dieter.

1) I do think the excess capacity story is a bit overplayed in the press, where the interests of producers based outside of China tend to be presented as fact. Of course, there is a serious cyclical and structural downturn underway in steel and other products for which demand is driven by domestic housing construction, and the production capacity of these industries has to adjust (and in fact is adjusting). But also see my post (https://andrewbatson.com/2016/04/19/is-steel-excess-capacity-a-symptom-of-chinas-system-or-of-its-size/) on how China’s size exacerbates this excess capacity problem: because China is so big, the world market is not large enough for China to maintain capacity utilization in steel by exporting, which a smaller country could do.

2) Quite possibly. It’s pretty obvious I think that China sets the global price for steel, the classical industrial good, which is something that steel producers outside China are not very happy about. This price-setting power is however probably also related to the fact that China is the main global consumer as well as producer of steel.

3) Tyler Cowen asked the same question, which is a good one that I did not consider at first. So I will just quote him (in a draft paper): “China, like most of the developing world today, is likely to undergo premature deindustrialization. … If there is a bright side to the Chinese situation, it is this: the country is so large, it has continued to diversify its manufacturing rather than specializing. If we look at the history of say industrialization in South Korea, at first the country produces all sorts of manufacturing goods, if only to drive its own growth. As the economy matures, it trades more for the most efficient inputs and thus home country manufacturing specializes more, namely domestic Korean companies specialize in what South Korea can sell effectively in global markets. Samsung and Hyundai persist, but the local manufacturer of diapers may or may not prove competitive. That is a natural pattern for smaller countries. In China, however, the country is still producing a wide array of manufacturing goods for the home market. The Chinese market is so large, and the value of direct access to that market is so significant, that China has not significantly specialized its exports the way many other developing nations have. That holds out some prospect for a relatively high level of manufacturing employment in China, looking forward.” I think it’s true that China’s size means it is possible for its domestic companies to achieve economies of scale that in other countries would only be possible by becoming a globally competitive exporter.