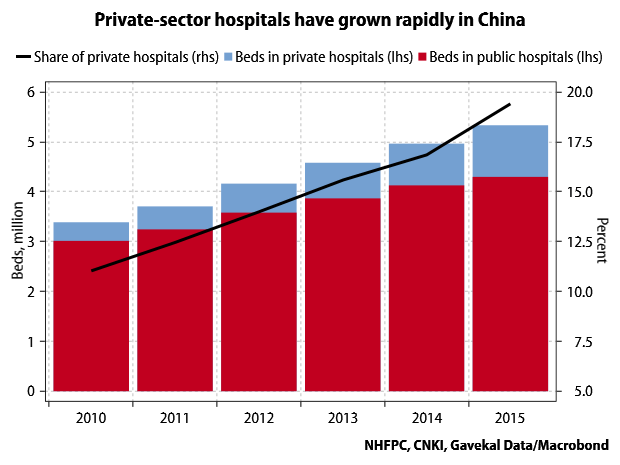

China’s new statistical communique on healthcare is just out, providing another snapshot of how the private sector is doing in this state-dominated field. Although the role of the private sector across the economy has not, unfortunately, increased much in recent years, healthcare has generally been an exception to this worrying trend since the reforms adopted in 2009. According to the communique, private hospitals accounted for 19.4% of hospital beds in the country as of end-2015, up from 11% in 2010, after they added nearly 200,000 new beds in the year. Private hospitals’ market share is probably a bit lower than their share of capacity, as they accounted for 14.7% of hospital admissions in the year. But both indicators represent pretty decent progress toward the goal, set in the 12th five-year plan on healthcare, to have private hospitals account for 20% of “hospital beds and service volume” by 2015.

I have argued that China could also adopt such targets for raising the private sector’s role in sectors other than healthcare (see this Q&A, and the full paper). And some domestic experts argue that the target for the private sector’s share of healthcare should be radically increased, in order to drive more decisive liberalization. The weight of establishment opinion appears to be swinging against these views, however, judging from a new report on healthcare reform, jointly produced by the Ministry of Finance, the National Health and Family Planning Commission, the Ministry of Human Resources and Social Security, the World Bank, and the World Health Organization. There is a lot in the report, but the section on the private sector’s role attacks the target fairly directly:

Quantity targets have spurred private sector growth in ways not consistent with national health objectives. …

It is worth noting that no OECD country has used quantitative targets to expand the private sector, but has rather employed a combination of supportive policies and regulatory structures that level the playing field with government-owned providers and assure alignment with health system goals.

Why has the expansion of private sector healthcare not been ideal from the perspective of the overall goals for healthcare delivery? Apparently because private sector hospitals are only serving a narrow part of the market:

Occupying a space created by the over-worked and crowded public system, the private sector offers alternatives to those seeking more and better medical products and services. However, despite central policies encouraging greater collaboration between public and private sectors, many local governments continue to focus their service planning and public financing on public service providers, effectively segmenting the market for the private sector for services targeting the wealthy and specialty facilities mostly offering elective services.

This seems to be a function of the fact that, despite setting a target for an increased role for the private sector, there are many unresolved regulatory issues for private hospitals and very uneven implementation of reforms granting them greater market access:

Despite the acceleration in recent years in the pace and scope of policies promoting private healthcare production and delivery, there continues to be no unified vision for the role of private providers in improving service delivery or contributing to national health objectives, and consensus has yet to be formed across government agencies on whether the private sector should be complementary, supplementary or integral to the public delivery system. …

The central government has enacted a rich set of national policies regarding private sector engagement, yet there are differing interpretations of these policies by provincial and municipal governments, among government agencies and between the public and private health sectors on the role of the private sector in contributing to national health objectives. From an implementation perspective the policy direction is unclear.

There is also a concern that the regulatory system is not keeping up with the changes, so it is ill equipped to address malpractice or other problems at new private-sector facilities.

The private sector requires a well-functioning governmental stewardship mechanism in order to grow, one that has the capacity of monitoring (and shutting down, as necessary) facilities seen to be endangering patient safety or defrauding social health insurance. Regulatory frameworks for accountability and quality assurance, however, exhibit wide local variations and are not uniformly strong. It is widely believed that private providers are more likely than their public counterparts to engage in false advertising, over-treatment, or fraudulent billing practices, and unsurprisingly, the private health sector in China does not have a good reputation with health consumers.

The report recommends a different but, I have to say, somewhat vaguer approach:

In keeping with the focus on quality development as against quantity growth, move away from quantity targets for private sector market share and instead employ a combination of supportive policies and regulatory structures that level the playing field with government-owned providers and assure alignment with health system goals.

It seems unlikely, then, that China’s next five-year plan for the healthcare sector will include a clear, quantitative commitment to a much larger private-sector role in the healthcare sector.