I have been happy to see Brad Setser return to the blogosphere, filling the giant hole his foray into public service had opened. In a recent post, he pushed back against the conventional concern about excessively high levels of investment in China to argue that there should be more focus on the issue of high savings:

A high level of national savings—national savings has been close to 50 percent of GDP for the last ten years, and was 48 percent of GDP in 2015, according to the IMF—creates an on-going risk that China will either over-supply savings to its own economy, leading to domestic excesses, or to the world, adding to the risks from global payments imbalances.

From this point of view, the high level of investment, and the risks that come from high levels of investment, flow in part from the set of policies that have given rise to extraordinarily high levels of domestic savings. …

So I worry a bit when policy advice for China focuses primarily on reducing investment, without an equal emphasis on the policies to reduce Chinese savings.

If I understand him right, Brad is worried that if China takes everyone’s advice and slows credit and investment growth, savings will not also slow down–and therefore the balance of payments will blow out, which the rest of the world would not be happy with. I think this is obviously true in the short term: investment can move quite quickly, while savings behavior seems to change more slowly. So a sudden slowdown in Chinese investment is unlikely to be smoothly accompanied by a similar adjustment in Chinese savings. But it seems like this would be the case in any sharp cyclical adjustment in investment, so fine-tuning policy advice to China might not make much of a difference.

Over the longer term though I’m not sure I am as worried as Brad is about continued high savings in China. Brad’s concerns I think arise from the view that high savings in China are driven by structural factors, and so a cyclical slowdown in investment will not affect savings that much. He is correct to note that national and household savings rates have not changed very much recently, so counting on them changing rapidly in the future does not seem like a good bet.

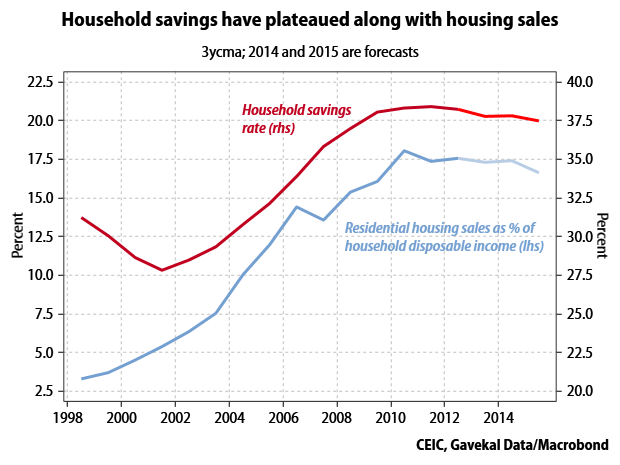

I agree that savings rates tend not to change very quickly, but I also think high savings in China are to some extent a cyclical phenomenon driven by high growth and large investment in housing. This view is in part based on recent research that emphasizes the role of demographics and rapid income growth in driving household savings (see this post); the hypothesis that stingy social welfare policies are the main culprit, because they induce lots of precautionary savings behavior, was conventional wisdom around 2003-04 but has not held up well. And in part it’s because I think the housing boom drove up savings and investment at the same time, rather than just providing an investment channel for already-high savings.

An excellent paper by Guonan Ma, which I have previously cited, is one of the best and most comprehensive statements of this housing-centric view; he estimates that household investment (ie, housing), accounts for most of the rise in household savings, which in turn accounts for most of the rise in national savings:

The household sector has been the largest driver of China’s gross domestic saving, accounting for around half in 2013 and generating nearly two-thirds of the rise in the national saving rate during the two decades for which we have flow-of-funds data. … the increase we observe in household capital formation can itself account for more than three quarters of the rise in household saving and thus could explain more than half of the reported fall in the household consumption during the 1992-2013 period.

A recent paper from the Kansas City Fed on Chinese consumption also endorses the view that savings rates were pushed higher by the housing boom of the first decade of this century:

The large jump in the household saving rate from 2000 to 2010 is largely related to development in China’s housing market during this period. Before 1998, most Chinese families lived in government-provided houses; after economic reforms in 1998 removed this benefit, however, most Chinese families needed to buy their own homes. This change triggered rapid growth in the Chinese real estate sector, causing home prices to rise tremendously. Furthermore, as house prices started to increase quickly, housing became a popular investment for wealthy Chinese households, raising demand even further and exacerbating house price increases.

As I think the housing boom in China is more or less over (it seems to have peaked, in volume terms, around 2011-12), I expect housing investment to slow and decline in the future. Savings motivated by housing investment should therefore also slow and decline. So the previous decade’s rise in investment and savings rates should naturally be followed by a decline in both investment and savings rates–rather than, as Brad fears would be the case, just the investment rate.