The following summary of a recent report on the size of the state sector in Russia is truly mind-blowing:

The state has rapidly increased its presence in the economy. Together with state-owned companies, its share in GDP rose from 35 percent in 2005 to 70 percent in 2015. The number of state and municipal unitary enterprises has tripled in the last three years alone, and they continue to appear in markets with highly-developed competition where their use of administrative resources and government financing poses a serious threat to other players. Such businesses have mushroomed at the regional and municipal levels, squelching competition in local markets.

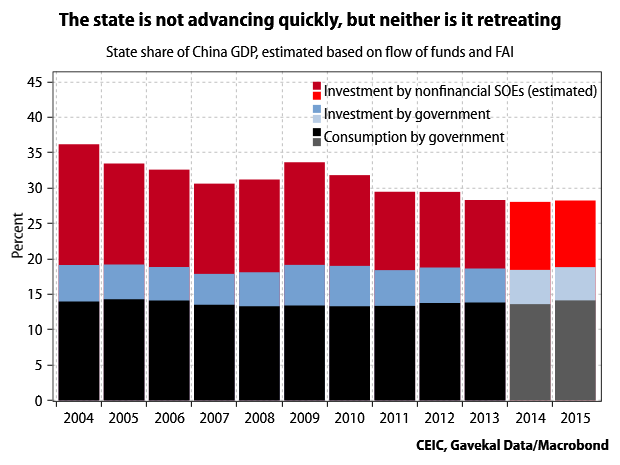

A 35% of GDP increase in the state (government + SOE) share of GDP over a decade is absolutely enormous. For all of the hand-wringing about the dire state of SOE reform and growing government intervention in China, it has seen nothing at all like this. Rather, China has gone from a positive trend of a declining state share of the economy in the 2000s to a less promising flat trend in the post-crisis yeas. My best estimate of the state share of China’s GDP is below (I use the flow of funds for government consumption and investment, and calculate gross capital formation by SOEs from the SOE share of fixed-asset investment; the flow of funds data only goes to 2013 so 2014 and 2015 are extrapolations). China and Russia seem to have had about the same state share of GDP in 2005, but since then China’s share has declined modestly:

Yes, that means that all of the huge amounts of infrastructure spending channeled through SOEs in recent years did not substantially increase SOEs’ share of the economy. Infrastructure is just not that a big a sector of the economy, and private investment in manufacturing is much more important (it’s true that the SOE share of the economy is not the same thing as broad government influence over the economy, but I’m sticking to things that can be measured at least approximately).

What has happened over the past several years is that private-sector investment, which previously was always much faster than state-sector investment, has slowed down substantially, while state-sector investment has picked up. As a result private investment is not growing much faster than state investment, and so the private-sector share of the economy is no longer rapidly rising. Nick Lardy explained it well at a recent presentation at a Peterson Institute conference:

The underlying problem or the underlying reality is that private investment growth relative to state investment growth has moderated quite a bit since 2011 and now has slowed down even more. … In part it’s because of the huge emphasis on infrastructure investment [carried out by state firms] and in part that state firms have gotten better access to what you might think of as external funding either on the form of bonds, bank credit, or the state budget. …

The rise of private firms, particularly the growing share of investment undertaken by these firms, has been a major driver of China’s economic growth in the reform period. While private industrial firms continue to dramatically outperform their sate counterparts, if the slowdown in private investment that we’ve seen so far in 2016 continues, I think it will be quite adverse for China’s medium-term economic growth.

This is definitely not a positive trend. But if the Russian numbers are at all accurate, something much more dramatic has happened there. The enormous rise in debt and distortion of the financial system that has occurred in China was sufficient only to stabilize the SOE share of GDP. So my guess is that it would be basically impossible for the state share of China’s much larger and more diverse economy to increase as much as Russia’s has, at least in the absence of radical expropriation. I guess that’s a good thing.