The below is from Paul Krugman’s latest on China, an argument also strongly endorsed by Brad Setser:

China really can’t keep investing 40-plus percent of GDP. It needs to shift over to higher consumption, which it could do by returning more profits from state-owned enterprises to the public, strengthening the social safety net, and so on. But it keeps not doing that.

Myself, I think it’s weird that people who want China to invest less tell it to do all these structural reforms rather than just, you know, invest less.

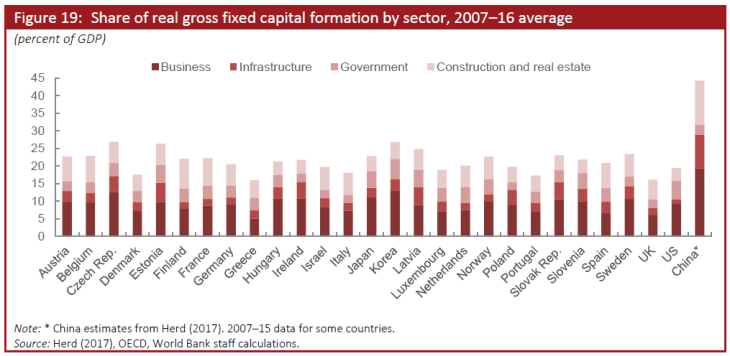

They miss the point that much of the low-return investment in China is done by the government and the state sector: it’s all those local infrastructure projects. That’s really where the buildup of excess investment is happening, not so much in the private business sector (which faces hard budget constraints and often tough access to credit). According to the World Bank’s latest China Economic Update, China’s public investment has averaged 16% of GDP since 1978, while OECD countries spend about 3.7% of GDP.

So if the government wanted to make a policy choice to invest less, it can just directly make the state sector invest less in those crappy low-return projects. It doesn’t have to overhaul social policy first.

The point of strengthening the social safety net, in this framework, is to reduce precautionary household savings. But high household savings don’t directly lead to excess investment. They do help keep the banking system liquid which enables a lot of borrowing by SOEs.

But trying to impose financial discipline on SOEs by improving the safety net and lowering household savings is pretty indirect. The central government could just require investment projects by SOEs and local governments to clear more hurdles.

Fundamentally, the reason that China invests a lot is that the government has made a decision to keep public-sector investment high in order to boost aggregate demand. If/when that changes, the investment rate will come down. And so will growth. Which is why China is not in a rush to make that call.

The hard choice that China has to make is not whether to undertake complex and difficult technical reforms to social policy. The hard choice is to decide when the efficiency losses from forced high investment start to outweigh the benefits of the boost to aggregate demand.

Some people are interpreting the government’s recent pledges to avoid “flood- like” (大水漫灌) stimulus as a sign that they have in fact reached this conclusion, and want to wean the economy off low-return infrastructure projects. Maybe a bit, at the margin. But the leadership is also going to a lot of trouble to create new funding mechanisms to ensure local infrastructure projects can continue, so it seems clear they don’t want this shift to happen right now.

Redirecting some fiscal resources from investment to consumption (i.e. more social programs) could certainly help soften the blow. But this is a compelling argument only to macro people; the Chinese interest groups that would lose out from less public investment are not going to feel compensated if more social benefits go to households.