China’s government has never been particularly shy about supporting its manufacturing sector, a key engine of growth for decades. Since 2021, though, it has become even more vocal about the importance of manufacturing, officially adopting in its plans the view that manufacturing is a special sector of the economy deserving of special treatment. That view may well be correct, and I have some sympathy for the argument. But the metric the government has chosen to measure its success is likely to prove a disappointment.

A good recent example of the new style of rhetoric around manufacturing is an article published in a recent issue of Seeking Truth, the Communist Party’s theoretical journal, by Jin Zhuanglong, head of the Ministry of Industry and Information Technology (MIIT). It does not break new ground but expresses the current line of thinking quite clearly; here are a few choice passages:

Industrialization is the precondition and foundation of modernization. … For a large country like ours, it will be difficult to achieve the goal of becoming a modernized superpower without a strong and large industrial sector. …

Industry is the main engine of economic growth, and plays a key role in stabilizing the overall macroeconomy. Industry is the main battlefield of technological innovation, it is the sector with the liveliest innovation activities, the most abundant achievements of innovation, the most concentrated applications of innovation, and the strongest innovation spillover effects. According to statistics, industry in the United States accounts for less than 20% of GDP, but 70% of innovation activities rely directly or indirectly on the industrial sector. …

We must hold fast to the real economy, especially the manufacturing sector, consolidate the advantages of a complete industrial system, keep the proportion of the manufacturing sector in GDP basically stable, and avoid the “virtualization” of the economy.

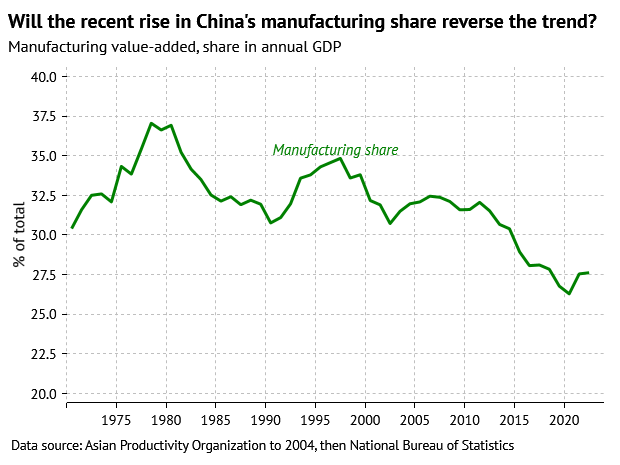

There are a lot of fairly abstract goals outlined in Jin’s article: many things that must be “improved” or “strengthened” in the common parlance of Chinese officialdom. The main one that can be actually measured is the manufacturing share of GDP; the goal of keeping that ratio “basically stable” was written into the 14th five-year plan.

That mandate is why, in the MIIT’s annual work conference in January, Jin proudly reported on the rise in the manufacturing sector’s share of GDP in 2022, to 28%. Such a shift in China’s economic structure is indeed a notable event, reversing a multi-year decline in the relative (not absolute) size of the manufacturing sector, which was over 30% of GDP as recently as 2014. But most of the change happened in 2021, when there was a simultaneous boom in both export manufacturing and in domestic demand, driven by property.

The property boom deflated in dramatic fashion in 2022, with historic declines in construction indicators. And while exports started off strong, by the end of the year they were declining, as China’s major export markets scaled back their spending on goods favored during the pandemic (furniture, electronics). The increase in the manufacturing share for the year as a whole was small, and higher-frequency data show it had actually begun declining by the end of the year.

China’s economic growth is universally expected to accelerate in 2023 thanks to the lifting of Covid restrictions, but a repeat of the 2021 manufacturing boom looks quite unlikely. Real-estate construction could pick up some, and with it demand for manufactured goods like steel, cement, and machinery, but a return to the boom years is not in the cards. While consumer spending in the US is solid, spending patterns are shifting to be less favorable to China (more services, fewer goods). A similar shift is likely to unfold domestically, with consumers splurging on the services, like travel, they have not been able to fully enjoy for three years.

It looks quite probable that manufacturing will lag rather than lead overall economic growth in 2023, resulting in a lower share of GDP. That may be why, at the latest MIIT work conference, stability in the manufacturing share was not mentioned as a specific goal for 2023, which it was for 2022 and 2021. There’s no point in emphasizing goals that are unrealistic.

Looking beyond the peculiar circumstances of 2023, I think it’s more likely than not that de-industrialization, meaning the decline of the manufacturing share of GDP, will resume. Rather than being an indication of the hollowing-out of the Chinese economy, as policymakers seem to fear, such continued structural change would probably be a fairly normal and neutral development.

The success of manufacturing in raising incomes in China naturally leads to some relative decline: as households’ incomes rise they tend to spend more on services, while at the same time Baumol’s cost disease raises the relative prices of services over time. Neither of those trends threatens the international competitiveness of Chinese manufacturing.

The manufacturing share of GDP stayed unusually high in China for decades in part because of typically socialist economic distortions: repressing consumer spending to channel investment into industrial capacity. Trying to maintain such distortions to prevent natural structural change could be quite costly in what is now a much larger, more marketized and globally integrated economy.

To really prop up the manufacturing share in an economy of China’s size would probably require extending the housing boom even further, or consistently undervaluing the currency, neither of which sounds like a great idea. My best guess is that China’s government won’t be able to stop a renewed decline in its manufacturing share of GDP, and, despite its rhetoric, won’t seriously try to.