As China’s data continue to disappoint, there is a persistent theme in much of the outside commentary on its economic woes: that China is for some reason failing to take the “obvious” step of sending stimulus checks to households. The implicit argument is that the US handed out massive subsidies directly to households, got a great post-pandemic recovery and everything turned out fine. China did not deliver subsidies to households, and that’s why everything is very much not fine.

Why is China, still, not taking this course in spite of the positive example of the US? Of course, an obvious answer is that the people in charge don’t think the US example was that positive, and anyway aren’t particularly prone to think of the US as a model to emulate. The merits of the pandemic fiscal-policy response are still pretty contested in the US. Plenty of people think of the stimulus as a fiscally irresponsible gamble that ultimately had pretty disruptive macroeconomic effects, because of the huge interest-rate increases that were required to bring inflation under control; my perception is that many people in China share these views. Still, the case for stimulus is probably getting stronger rather than weaker at the moment as China falls further away from potential growth and full employment.

My suspicion is that part of Chinese policymakers’ reluctance to use direct transfers to households as a short-term stimulus stems from a fear of setting a fiscally destabilizing precedent. If debt-financed transfers failed to generate a sustainable recovery, the money would be wasted. But if transfers succeeded in generating a good burst of growth, that could have even bigger longer-term effects. It would mean that, the next time China falls short of potential growth and full employment, the political pressure to roll out household transfers again would be overwhelming. What started as a one-off policy response could become entrenched as the expected response to any growth slowdown, and would add to government deficits and debt over many years rather than just one.

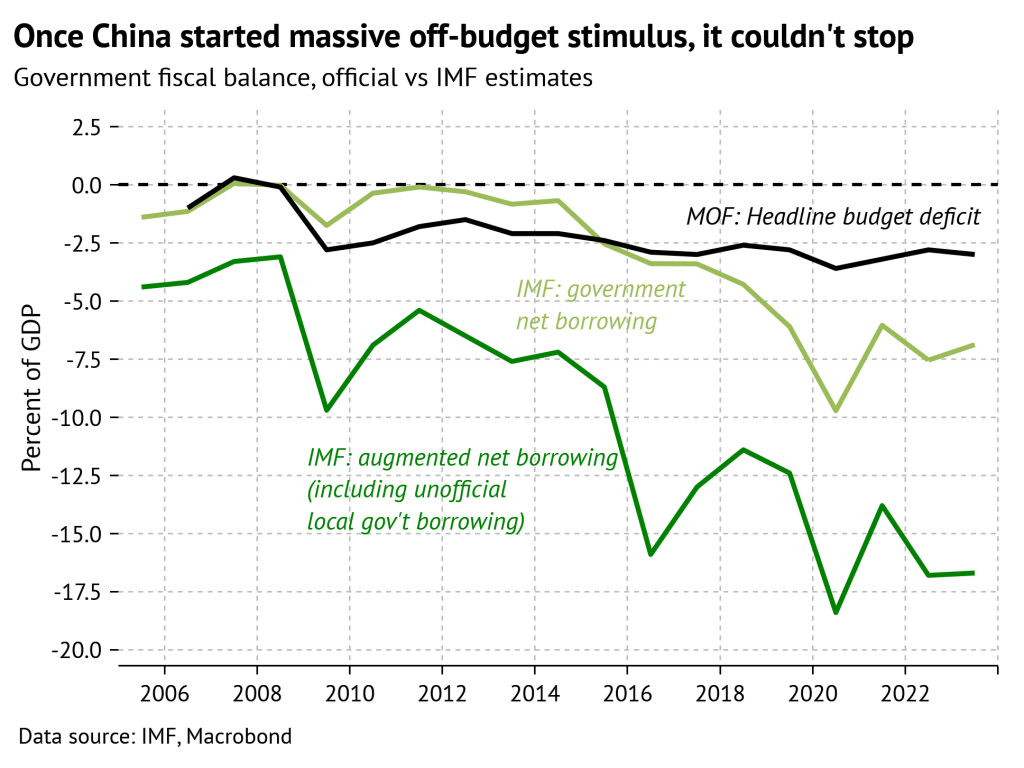

Why should this hypothetical possibility be a serious concern for Chinese policymakers? Because it is exactly what happened after the 2008 financial crisis. An unprecedented global shock led to an unprecedented policy response, as the central government encouraged local authorities to use off-balance-sheet borrowing to fund a wave of public works projects. If that had been a one-off measure, it would have been a powerful example of effective and unorthodox policymaking. Instead, the infrastructure stimulus institutionalized fiscal irresponsibility on a massive scale: a decade and a half on, the off-balance-sheet local borrowing is even bigger relative to the economy than it was in 2008, according to IMF estimates. It would be hard to find a better example of Milton Friedman’s quip that “nothing is so permanent as a temporary government program.”

China’s political system therefore does not have a good track record of being able to take away the punch bowl in good economic times in order to be able to share out more punch in the bad times. The dubious legacy of the 2008 stimulus means that China now needs fiscal consolidation to get long-term debt dynamics under control–at exactly the moment that it once again faces a shortage of aggregate demand.

Striking the right balance between the structural and cyclical issues is indeed quite difficult. Maybe the right answer is in fact that the cycle needs more attention at the moment, because a failure to address the loss of growth momentum would allow hysteresis to set in and create even more long-term costs for the economy. But it is perhaps understandable that the people inside China’s system are reluctant to experiment with new forms of fiscal stimulus before they have gotten the old ones under control.

Excellent

But a permanent program to tax capital income, capital gains inheritances and property, which used the proceeds for income redistribution, might permanently boost consumption given the extremely high saving rates of the top 10% and the concentration of capital income.