In June I went to India for the first time. It was a quick trip, just a week, but I still got a pretty intense introduction to current debates on the Indian economy at the India Policy Forum in Delhi. As a China specialist with only a newspaper-reading level of familiarity with India, I was quite intimidated by the prospect of joining a roomful of people who have spent their entire lives working on tough economic questions of India. It turned out, though, that if you’re going into the equivalent of a high-level graduate seminar on Indian economics as an outsider, having a background in China is not the worst preparation. Almost every paper and every talk about India’s economic problems seemed to be motivated by some implicit comparison with China.

At first I thought I was over-interpreting things because I am biased to look at things from a China perspective, so I asked around to check my perceptions. The answer was: Yes, all this is in fact about China. It’s because the Indian elite has assumed for decades that India is destined to be the next global economic superpower after China, so the overriding question for them is why that hasn’t happened and what needs to be done to make it happen. The comparison with China seems to revolve around a number of generally accepted stylized facts, which form the basis for identifying policy issues and posing research questions. To me (as, again, an outsider to these debates), the key ones seemed to be around manufacturing, investment, human capital and state capacity.

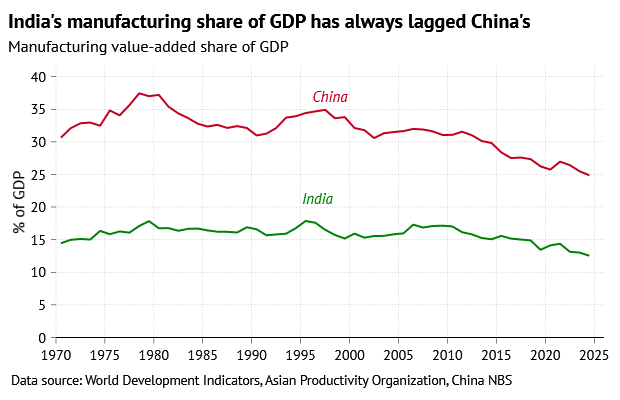

One of the most obvious economic contrasts between India and China is that China has followed the East Asian model of export-led manufacturing, like Japan, South Korea and Taiwan (albeit at much greater scale), and India has not. All of those Asian economies historically had high manufacturing shares of GDP, and while in all of them the manufacturing share is lower today, it is still higher than in India. In recent years India’s manufacturing share of GDP has been around 13%, about half of the level in China, and historically it has never exceeded 18%. One of the central debates among Indian economists is how much of a problem the relative weakness in manufacturing is, and what should or could be done about it.

Historically, it is definitely true that manufacturing has been a key motor for structural transformation away from traditional agriculture to modern production based on wage labor and economies of scale. And the reason many Indian economists worry about the low manufacturing share is that it seems to be a symptom of slow structural transformation: the agriculture share of GDP and employment has remained largely static in recent years. So while the modern sector in India’s economy is clearly growing, it doesn’t seem to be pulling workers out of the traditional sector, limiting the income gains. That concern is behind proposals to encourage the growth of labor-intensive manufacturing.

India’s government has also set explicit targets for the manufacturing share of GDP: the “Make In India” initiative back in 2014 called for pushing up the manufacturing share to 25% by 2022, which obviously didn’t happen. NITI Aayog, the public-sector think tank that has replaced the old Planning Commission, is still talking about a 25% target, this time for 2047, the centenary of India’s independence. It is worth noting that China has, in fact, never set a quantitative target for the manufacturing share of GDP. Currently the government just talks about “maintaining basic stability” in the manufacturing share, which hasn’t stopped it from declining.

It’s also interesting that a recent comparative study of China, India, Indonesia, Mexico, and South Africa emphasizes that transitions out of agriculture played a limited role in raising household incomes out of poverty; income gains within sectors often played a larger role than reallocation among sectors. Which is not to say that more structural transformation of the economy would not be helpful for India, but perhaps it is not right to get hung up on the relative shares of different sectors. After all, there’s no economic theory that can tell India what its optimal share in GDP of manufacturing should be. You can’t treat shares of GDP like temperature readings, and use naive cross-country comparisons to say, oh, this level is obviously too low, there’s a deficiency, or this level is obviously too high, there’s an excess.

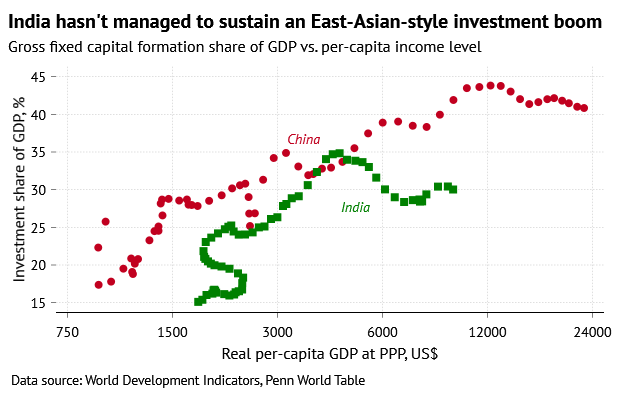

A closely related contrast between India and China is its relatively lower investment share of GDP. One assertion I heard, which received broad agreement, was that no country has been able to successfully develop without sustaining an investment share of GDP of over 30% for decades. This is based on the East Asian development experience: Japan, South Korea and Taiwan, as well as Malaysia and Singapore, all sustained 30%-plus investment rates for long periods of time, alongside their higher manufacturing shares of GDP. China of course, is the investment champion, for better and for worse, keeping its investment share of GDP consistently over 30% since 1992, and over 40% for the past 15 years. Again, China is implicitly (and often explicitly) the point of departure for the Indian debate. A World Bank report this year endorsed a “reform” agenda to push India’s investment share of GDP to 40% by 2035.

India’s investment share of GDP is actually not that low: it’s been around 30% in recent years, and was over 30% for roughly the period of 2005-13. True, this does not quite meet the (perhaps arbitrary) historical threshold for an East Asian-style investment boom. And some Indian economists express concern that the recent pickup in investment is aided by large public-sector investment in infrastructure, which may not be sustainable, and that private-sector corporate investment has been static or falling as a share of GDP. While corporate profits have been strong in recent years, they report that the weakness of private-sector investment seems to be concentrated in manufacturing: companies just do not see good prospects for adding manufacturing capacity. If India does not have a manufacturing boom, it probably will not have a broader investment boom.

An alternative view expressed by some other economists is that India is already growing rapidly with a 30% investment rate, the current returns on services investment are high, and it’s not obvious that it needs to push a lot more investment. I found myself sympathetic to this side of the debate. China today, after all, is hardly a model to follow: it has experienced massive excess capacity and declines in returns on capital since the 2008 global financial crisis, largely due to forced public-sector investment.

Still, China’s current excess investment is a product of both its peculiar quasi-socialist institutions and particular historical circumstances, neither of which have very close analogues in contemporary India. If India can find productive uses for a few more percentage points of GDP worth of investment, that would probably be welcome, and would hardly put it on the path to Chinese-style excess. But equally, it’s hard to take a simple cross-country comparison as sufficient justification for massive macroeconomic interventions to push up the investment share.

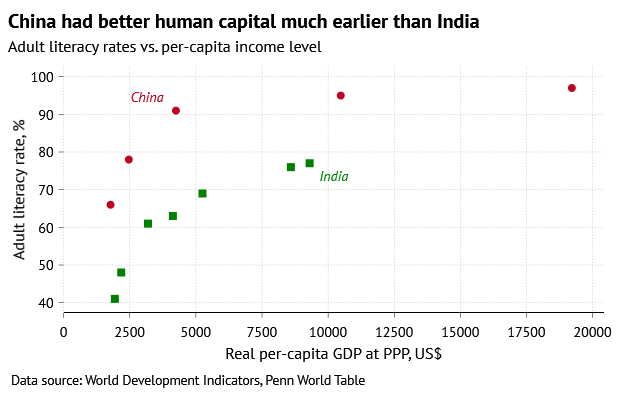

A more supply-side perspective on India’s relative dearth of manufacturing and investment focuses its failure to establish the necessary social preconditions for an East Asian-style growth takeoff. As Wang Feng’s recent book China’s Age Of Abundance emphasized, China was able to seize the opportunity presented by labor-intensive export manufacturing in the 1980s because it had made substantial improvements in health, education and gender equality in prior decades. China’s workforce already had the necessary human capital to transition effectively to jobs in the modern economy, when reforms started to make those jobs available.

In terms of some basic measures of human capital, India has yet to catch up to where China was decades ago. According to the World Bank, India had an average adult literacy rate of just 77% in 2023–roughly China’s level in 1990. This average gap is aggravated by the scandalously low female literacy rate in India, just 70%. (Other measures like average years of schooling also show a gap). One reason why manufacturing has not taken off in India may well be that India does not have a mass workforce equipped with the basic skills to perform manufacturing jobs.

The low average endowment of human capital in India is striking given the high achievements of the most educated: India obviously does have a workforce equipped to perform high-skilled jobs in information technology and services. A recent paper by Nitin Kumar Bharti and Li Yang collects a remarkable amount of historical data to show substantial differences in educational priorities between India and China. After independence, India invested more in university education but neglected primary and secondary education, producing a relatively small cohort of skilled graduates amid a large uneducated and illiterate population. China, by contrast, initially focused on achieving broad-based basic education before emphasizing the expansion of university education after the 1980s.

Bharti and Li document that India has since the 1990s tried to expand enrollment in primary and secondary education, which is reflected in rising literacy rates. But the quality of basic public education still seems poor, and more education spending is not always producing better results. There are lots of shocking stories about widespread teacher absenteeism and incompetence. It is generally reported that higher-income Indians will do whatever they can to stay out of the public education and healthcare systems. This points to an even more fundamental contrast between India and China, which is in state capacity: the government’s ability to get things done.

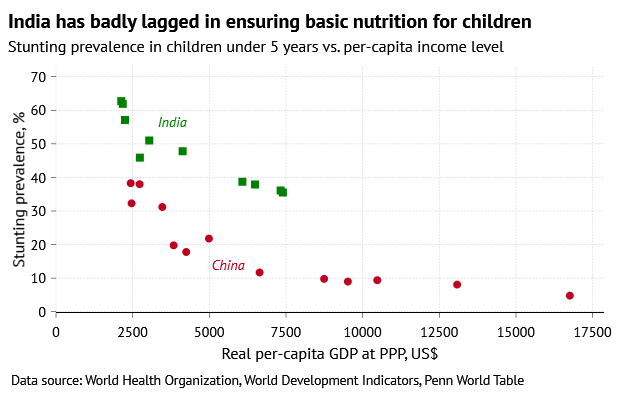

In particular, India’s government seems to struggle to deliver basic public services and provide a baseline level of human welfare. Another fact about India that is, deservedly, often repeated is its alarmingly high proportion of underweight and stunted children. The last survey data collected by the World Health Organization show that 36% of young children in India were stunted (far too short for their age) in 2020. That’s similar to the proportion in China in the mid-1980s; but China at the time had per-capita GDP of only a third of India’s today. An interesting case study of Karnataka, one of India’s most developed states and home to the IT hub of Bangalore, reinforces the point. While Karnataka has had one of the best growth stories in India, it has still a higher proportion of children who are stunted, underweight or not enrolled in school than some poorer states. The significant increase in economic resources available to the state government does not seem to have translated into better outcomes for much of its population.

One set of these comparisons and stylized facts, those on manufacturing and investment, are frequently used to argue for more aggressive efforts to transform India’s economy and put it on something more like a Chinese (or East Asian) trajectory. But the other set of comparisons, on human capital and state capacity, implicitly counsel caution. If India does not have the necessary preconditions for a manufacturing takeoff, companies probably would not respond strongly to government favoritism for manufacturing (and indeed most people seem to think the response to the Make In India initiative has been underwhelming). In any case, a government that struggles to deliver basic public services is unlikely to be able to execute interventionist industrial policies effectively. Even China has plenty of waste and corruption scandals alongside the success stories.

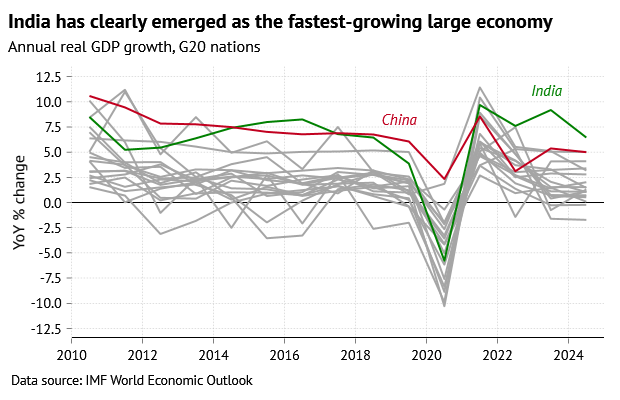

Yet it is also worth emphasizing that India does not come off the worse in all comparisons with China. It’s an important fact that, since the pandemic, India has overtaken China to become the world’s fastest-growing large economy, averaging real GDP growth of over 7%. This is all the more remarkable given that India clearly is not having an East-Asian-style boom in manufacturing and investment. Therefore, it must be having some other kind of boom: one led by services. The IT outsourcing wave, which got started in 1985 when Texas Instruments opened a research center in Bangalore, seems to have stepped up to a new level in the last few years, possibly boosted by the post-pandemic changes in working patterns. Foreign investment clearly plays a big role in this process, and I saw huge swathes of new office parks going up outside Delhi, adorned with multinationals’ names.

Given that, by general consensus, India has not solved its outstanding problems in agriculture and manufacturing, the fact that the services boom is strong enough to power 7%+ aggregate growth is pretty impressive. It’s hugely important that India now has a self-reinforcing growth cycle in foreign and private-sector investment and exports. It’s almost reminiscent of what happened in China in the 2000s after its WTO entry, even if India’s cycle is mostly in services, which have fewer spillovers to the rest of the economy than manufacturing. If there is an alternative school of thought to the one focused on trying to “be like China” in terms of macro aggregates, it is that India should focus on building on what is already working. That means not just facilitating the tech boom, but also making more sectors outside IT services attractive to investment from both domestic and foreign businesses, and trying to steadily improve state capacity and public services.

Incremental reforms might be more politically realistic than trying to drive a “big push” in manufacturing investment. Most of the commentary I heard in Delhi was pessimistic about the outlook for big policy changes, since the current fast GDP growth sends a signal that things are going well, and makes disruptive and politically costly reforms seem less necessary. But it is also true that evidence-based comparisons with China should be able to motivate lots of different ideas about what India can do: China itself has gone through lots of changes, and the growth model has been quite different at different points in time. There are a lot of people these days who think “being like China” means “doing manufacturing-heavy industrial policy,” but this is a perspective distorted by the particular set of government priorities since 2015 or so.

China’s turn to aggressive industrial policy came only after it had already become a quite successful export manufacturer. And that turn was explicitly justified on grounds of national security rather than promoting growth. It was precisely because China was already quite developed that it could afford to put lots of money into import substitution and speculative technological bets. The industrial-policy apparatus of today’s China is a completely inappropriate model for India, which faces a very different set of problems with a different set of capabilities. A focus on removing impediments to a private-sector-led expansion would in fact make India more like China–just the China of a different, less statist era.

If India averages 5.7% real GDP growth going forward, with 2.5% annual currency depreciation and adjusting for inflation, it would reach China’s current GDP level by 2075. However, sustaining 5.7% growth will be difficult (5.7% was India’s average from 2015 to 2024) and such rates will slow as the economic base grows. If we instead assume a more conservative 4.7% real growth rate under the same currency and inflation assumptions, India would reach China’s 2025 GDP level by 2098. In short, it’s misleading to compare the two economies as if they share the same growth potential.

>India has overtaken China to become the world’s fastest-growing large economy, averaging real GDP growth of over 7%. This is all the more remarkable given that India clearly is not having an East-Asian-style boom in manufacturing and investment. Therefore, it must be having some other kind of boom: one led by services.

I’m surprised you don’t consider another explanation, which is that the reported number is bogus. Not just a crank claim, either—the former Chief Economic Advisor to the Government of India wrote a paper alleging it (“India’s GDP Mis-estimation: Likelihood, Magnitudes, Mechanisms, and Implications”). India’s former chief statistician Pronab Sen also cast doubt on the GDP figures in an interview. The Indian government also stopped doing household consumption surveys for a decade since 2011 and the 2017 survey was not released owing to “data quality issues”—it allegedly revealed a fall in consumption.

I remember this paper making a splash when it came out in 2019, but there has yet to be much of a follow-up. If the claim were true, there are many correlates of GDP that would be off (e.g. earnings, exports/imports, electricity consumption, nighttime lights), especially as compounding takes effect. I find it hard to believe that the private sector and think thanks, both Indian and foreign, would all naively believe fabricated data for years and years and not notice it.