After spending a few weeks in Beijing, the general relief people feel at being out from under the hammer of Covid controls and having daily life resume is palpable, and also quite enjoyable. Less positive is the sense I get in many conversations of a lingering, deeper uncertainty about the direction China is headed. Impressions of this sort are admittedly fuzzy and intangible. But I think in this case, the uncertainty people feel has direct and visible causes, rooted in the fundamentals of China’s political economy.

My basic theory of how China works in a very simplified and top-level sense is that the Communist Party leadership sets goals toward which the nation is to strive, and cadres throughout society and the government mobilize in an attempt to achieve those goals. For the best part of four decades, the mobilizational goal was economic growth. In 2017, Xi Jinping declared, in the most formal, explicit and public way possible, that growth would no longer be the goal toward which the nation would mobilize (for a fuller exegesis, see my old post “Mobilization and modules: what’s changing in China“).

By doing so, he introduced a profound instability into the system. Xi’s proposed replacement for the goal of growth –“a better life”–was so vague and content-free, even by the low standards of Communist slogans, that it offered no coherent guidance for what officials should actually be doing. In practice, it seems to have meant listening to whatever the big guy’s political obsession of the moment was. This instability was exposed in 2021, when Xi rolled out a seemingly never-ending series of regulatory crackdowns and campaigns. The resulting market chaos largely discredited his new everything-but-growth approach, at least among a segment of financial elites. In 2022, the Shanghai lockdown and the repeated, confusing waves of Covid controls in the rest of the country arguably discredited it among a broader swathe of the populace.

What Xi has been up to since the two pivotal events of late 2022, the Party Congress in October and the reopening from Covid controls in November, is in my interpretation pretty simple: he is trying to re-establish a mobilizational goal for the whole political system after that breakdown. A lot of people hope that a chastened Xi will go back to the old mobilization strategy of economic growth first, everything else second. I am pretty sure that is not happening, despite the supposedly “pragmatic” and business-friendly approach of the new leadership team installed at the Party Congress, and the clear near-term focus on stabilizing the economy (see my post “Pragmatism as ideology” for the complete version of why I don’t buy this).

However, I also don’t agree with the default China-cynic interpretation that Xi is just biding his time before launching another 2021-style wave of rectification campaigns. I think the damage to the central government’s public support and ability to execute policy during the last days of Covid lockdowns was actually quite serious (see my post “Interpreting China’s policy reversals” for more speculation about what was going on then). Xi is nothing if not fully committed to preserving Communist Party rule, and has repeatedly shown he is willing to change course and abandon previous priorities in service of this larger goal. What hasn’t been clear is just what lessons he learned from the past couple of years and how those lessons will be integrated into his larger ideological project.

After a round of top-level meetings and propaganda signals in late April and early May, the direction Xi has chosen is coming into view. I think we now have a much better sense of just what he is proposing as the system’s new mobilizational goal. As befits a good Marxist, he has avoided a forced choice between thesis (the Dengist growth-first approach) and antithesis (the 2021 politics-in-command mode) and instead come up with a synthesis of both. The key organizing concept in the latest propaganda is the “modernization of the industrial system,” a concept that combines a practical focus on economic realities with Xi’s signature concerns of national security and geopolitical competition with the US.

In the readout from April’s Politburo meeting, a call to “accelerate the construction of a modernized industrial system that supports the real economy” (加快建设以实体经济为支撑的现代化产业体系) features as part of the answer to the economy’s near-term difficulties. ““Economic growth is better than expected, and market demand has gradually recovered… But the positive turn in the economy is still mainly restorative; internal dynamism is not strong, and demand is still insufficient.” The idea seems to be that intensified industrial policy will help develop “new growth drivers” that will attract private-sector investment. For instance, the meeting called for stepping up support for electric vehicles, an area where industrial policy has had notable successes, as well as for artificial intelligence, an area where the results are so far more mixed.

A few days later, the first meeting of the Central Committee on Financial and Economic Affairs focused on the same concept, while offering more big-picture guidance. This body, one of the suite of high-level commissions chaired by Xi, typically meets once or twice a year to set economic priorities. Its meetings in 2021 focused on internet platform companies and the “common prosperity” agenda of tackling inequality, the key elements of the anti-growth agenda that spooked financial markets. In that context, it is highly significant that the communiqué says high up that “economic development is the Party’s central work” (会议指出,经济建设是党的中心工作). That is exactly the kind of language that adherents of the old, growth-focused order have been hoping would be restored.

Yet the rest of the communiqué makes clear that there is no return to the previous paradigm. Economic development is needed not because it makes people better off, but because it makes the nation great: Xi said at the meeting that “a modern industrial system is the material and technological foundation of a modern country, and the focus of economic development should be placed on the real economy to provide solid material support for China to realize its Second Centenary Goal.” That goal is the one Xi has laid down for China to become a “modernized socialist superpower” by 2049, the centenary of the founding of the People’s Republic.

To achieve modernization requires “building world-class enterprises” and “cherishing outstanding entrepreneurs,” the meeting declared, but their efforts are still ultimately in service to the national project. “Modernizing the industrial system…concerns whether China can take the strategic initiative when it comes to its future development and global competition.” A few key adjectives flesh out what such a system would look like: it must be “complete,” meaning that all segments of the value chain are within China’s borders, or under its control; “advanced,” meaning that China has a strong position in high technology, and “secure,” meaning not vulnerable to external shocks or threats.

At the level of rhetoric, all this is a clever synthesis of many of Xi’s favorite themes. In the new conception, the pursuit of national security, technological self-reliance and higher global status is not separated from the pursuit of economic growth, but integrated with it. The strengthening of the nation’s entire economy against US sanctions and other external shocks is a massive undertaking that will demand major investment projects and create lots of opportunities for domestic companies. The vision is of the entire nation united in a common undertaking that delivers both prosperity and security.

Compared to the highly politicized “better life” agenda that Xi offered up in 2017, “modernization” is a more concrete and also probably more attractive goal. At least implicitly, concessions are being offered to critics of the recent missteps: the government is clearly committed to ensuring a strong economy, supporting private businesses and attracting foreign investment.

Xi’s unrepentant nationalism and tough stance with the US have generally been the most broadly popular part of his agenda, supported by many people not otherwise enthusiastic about his political campaigns. A clear and more broadly acceptable mobilizational goal for China’s Leninist political system will help reduce uncertainty and instability. And in most any system, to lop off the less popular parts of an agenda, focus more on the popular bits, and deliver practical results on the economy is good politics.

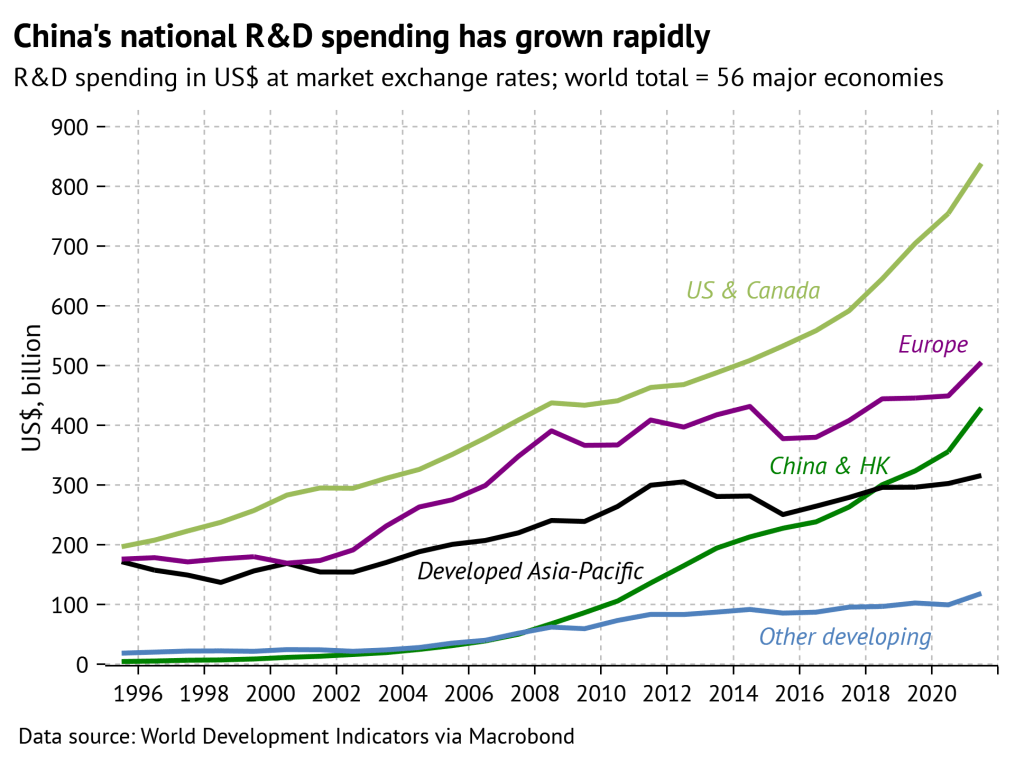

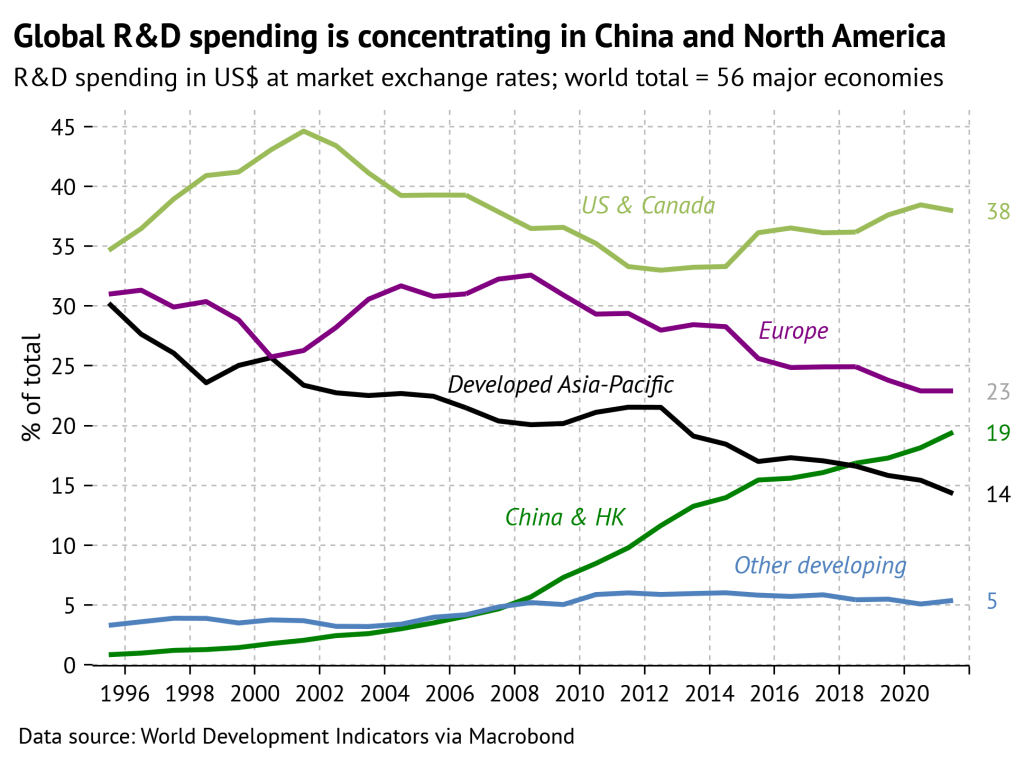

Below the level of rhetoric, it is less clear what all this means in practical terms. China’s bureaucracy has for years now been directed to deliver a heightened focus on national security, industrial policy and technological self-reliance. Credible estimates suggest China already spends far more on industrial policy, in both relative and absolute terms, than any other major economy. Actually, if the new agenda does not require radical alterations of existing policies and programs, that is another point in its favor. But if Xi is planning to double down on those efforts, that would really push China’s economy into uncharted territory.