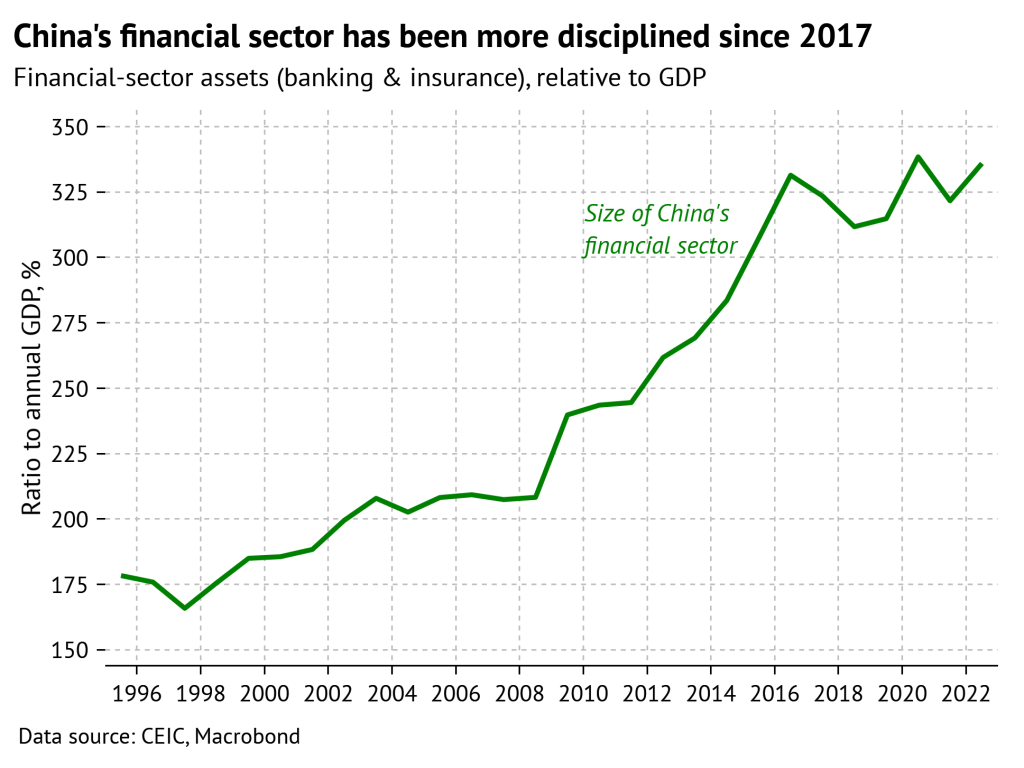

China’s most consequential economic policy of the last several years, aside of course from the Covid lockdowns, was its turn to increased financial discipline. In the decade after the 2008 global crisis, the financial sector had exploded in size, but in 2017 that growth came to, if not quite a halt, then a very obvious inflection point. As the chart below shows, the size of China’s financial sector relative to GDP has been roughly stable since then (the spikes in 2020 and 2022 were due to sharp slowdowns in the growth of the denominator rather than accelerations in the growth of the numerator).

The new direction was signaled at the end of 2016, and then really got going after Xi Jinping made the Politburo attend a study session on financial risk in early 2017. At the meeting he declared that “financial security is an important component of national security,” launching a campaign against financial risk in a way that made it a top political priority rather than a matter of mere technical management. Since then, the government has been remarkably consistent in holding to a tough, conservative stance on monetary policy and financial regulation.

Although no Chinese official would express it this way, essentially what happened in 2017 is that China started doing what the IMF and similar worthies had been telling it to do: control debt, close regulatory loopholes, impose hard budget constraints. This was a pretty unexpected move for Xi, who up until that point had focused his attention more on foreign policy, security issues, propaganda and ideology. It was also a pretty unexpected success for the technocratic types who had been warning about the dangers of rising debt for several years, to little effect.

This episode in Chinese economic policymaking is still not well understood. Why did the people usually identified in the Western press as “market reformers” focus their energy and political capital on this issue of financial discipline? And how were they so successful at getting their agenda adopted at the highest levels? Maybe one day when the principals write their memoirs we will know the real story.

But until then, I have some theories–or, at least, speculations. Even in a top-down system like Xi-era China, major policy decisions usually need buy-in from a range of interest groups. My speculation is that there are two major interest groups that aligned in support of this new agenda of financial discipline.

Let’s call the first group the “reform faction.” These people are indeed concerned that the surge in debt after 2008 has raised the risk of a financial crisis in China. But they also see the easy availability of credit as encouraging the worst features of the Chinese economy: the continued large role of state-owned enterprises, and the corrupt and unhealthy relationship between property developers and local governments. Imposing more financial discipline on these actors will thus help push the economy in the direction of higher productivity and a larger private sector.

Let’s call the second group the “control faction.” Their diagnosis of China’s problems is almost the opposite of the reform faction’s. Rather than seeing easy credit as enabling the dominance of inefficient state enterprises, they see it as enabling the aggressive expansion of corrupt and unaccountable private-sector companies. The huge concentrations of private wealth created by booms in property and the internet undermine China’s governance and challenge the authority of the Party. Imposing more financial discipline on these actors will reduce social and economic polarization and allow for healthier growth.

The ideals of these two factions are almost diametrically opposed. However, both can agree that the lax post-2008 policies caused a lot of problems, and that tighter central control of the financial system will help address these problems. The consensus policy is to impose financial discipline on both the private sector and the state sector, not just one or the other. For me, this model helps account for some of the internal contradictions of the financial crackdown–how it married a seemingly technocratic agenda with a socialist political campaign–as well as for its surprising toughness.

An unholy alliance between the reform faction and the control faction does not sound like an inherently stable configuration. Indeed, the indications are that the balance of interest groups is now shifting. All the top officials who implemented the financial crackdown are headed for retirement due to age. Recent corruption probes have implicated senior officials at the central bank and financial institutions. And the government has just announced a wide-ranging restructuring of the entire financial-regulatory apparatus.

Even if my model is wrong (as it quite likely is), the political economy around financial regulation in China has clearly shifted. Whatever was the actual balance of personalities, interests and agendas that supported the turn to financial discipline in Xi’s second term, it will be different for his third term.