A new Nick Lardy book comes along regularly every few years, and each one is an event for the China-watching community. Anyone who cares about the Chinese economy will find The State Strikes Back: The End of Economic Reform in China? interesting and provocative. This is a preview, not a review, since the book is not officially out until next week and so my Kindle pre-order hasn’t downloaded yet. But I saw his book talk in Seattle last night, where he gave a characteristically clear and concise summary of the argument (he also has an op-ed in the FT.)

The new book has to be understood in the context of Lardy’s previous book from 2014, Markets Over Mao: The Rise of Private Business in China. In that book he argued that it was the rise of increasingly efficient and productive private-sector companies that has driven China’s economic growth over the last four decades, not state-owned enterprises, government planning and industrial policy. In contrast to the view in some quarters that China remains a fundamentally state-controlled economy, he laid out all the ways in which markets have been liberalized and competition increased since 1978.

A lot of the key changes in the relationship between the state and private sector happened in the 1980s and 1990s, and are well explained in that book. But Lardy also engaged with the argument that, as he put it, “state-owned firms returned to prominence of the decade of leadership of President Hu Jintao and Premier Wen Jiabao (2003-12)”.

While acknowledging that the Hu-Wen government wanted to make state enterprises and industrial planning play a a bigger role in the economy, he argued that the data showed they had not succeeded. In fact, the private sector’s share of economic aggregates had continued to increase, not because of continued privatization but because private firms are more efficient and grow faster than SOEs. This process was aided by a substantial increase in private firms’ access to bank credit.

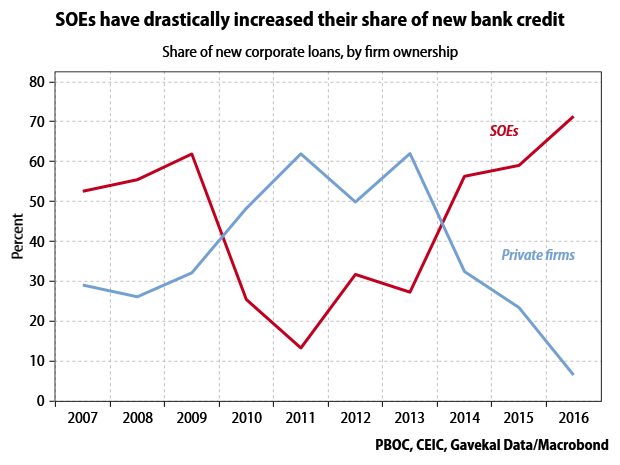

The main point of Lardy’s new book, based on his slides and talk, is that the positive trends he had emphasized in his last book are now going in reverse. The data now show that private firms’ access to bank credit has sharply declined, and that their share of various economic aggregates is also falling. He puts particular emphasis on the drop in lending to private firms:

(Note: Lardy has a chart like this in his slides, but this is my chart not his. It is based on the same underlying data but my estimates come out slightly different.)

The big decline in bank lending to the private sector (the absolute volume of new loans to private companies shrank, not just the share) had major consequences. It forced private firms to rely even more on shadow finance. But in 2016 the government also decided (correctly) that the rapid expansion of shadow finance posed systemic risks. The tightening of regulation led to an outright decline of shadow financing in 2018, putting many private firms into dire financial straits. The financial pressure on private firms has allowed their state competitors to expand at their expense: SOEs in industry are growing faster than their private competitors. Lardy said this is the first time this has happened since 1978.

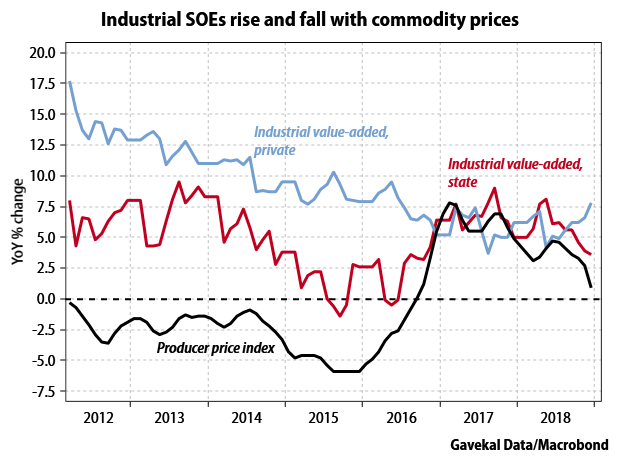

(Again, this is a re-creation of one of Lardy’s charts using public data.)

Lardy thinks all this is bad for China. He is right! He also puts most of the blame on the policies of Xi Jinping–tolerating SOE inefficiency, encouraging the creation of larger SOEs, tightening Party control over private firms–since these trends in the data did not show up until a few years into his administration.

Essentially, both of Lardy’s recent books are about the use of economic data to support a narrative about the direction of reform in China. In Markets Over Mao, he argued that the data did not support a narrative of the resurgence of the state sector, and in fact supported a narrative of the rise of the private sector to new heights. I think it is fair to say that a number of people felt that Lardy in that book was too forceful in downplaying trends that were in fact important, but perhaps were difficult to tease out in the aggregate economic data. Now, Lardy is arguing that the data support a narrative that the state is resurgent and the private sector is losing out. Since this is a recent reversal of a positive long-term trend, he thinks that if China changes course it could significantly boost its economic growth rate, by as much as 2 percentage points.

My own view is more that economic policy under Xi Jinping represents an intensification of trends that were already playing out under Hu Jintao. I think this is pretty clear if you pay attention to China’s official rhetoric and try to understand the underlying political economy. Since I think the problems go back further than 2015, I am less optimistic than Lardy about China’s longer-term growth prospects (thanks to Greg Ip of the WSJ for including a summary of my views in his latest piece).

I also think that it is tricky to tell a clear story about the rise or fall of the state sector using the official economic data–having spent a lot of time and effort trying to do that myself. As someone who very much appreciates Lardy’s careful work with Chinese data, let me offer a couple of caveats to the charts above, in the spirit of seeking truth from facts.

First, on the bank lending data. Lardy is right to highlight the sharp downturn in lending to private companies in 2015-16. But it is not clear to me that this is a result of government policy to favor SOEs. Recall that there was a pretty serious economic downturn in 2014-15. It would make sense for banks to respond to that by trying to reduce the risk in their loan books, and one obvious way to do that would be to curtail lending to smaller and riskier companies, i.e. private ones. (The fact that SOEs are seen as less risky than private companies is a structural problem, but it’s nonetheless true that banks are correct to make this judgment given the realities of China’s political economy.) In other words, the change may have been more cyclical than structural.

There is some preliminary evidence that supports this interpretation. The data that Lardy and I use to calculate lending to state and private firms is released with a long lag, and recent figures aren’t out yet. But banking officials disclosed last year that lending to private firms totaled 30.4 trillion renminbi as of September 2018. This is equivalent to 38% of outstanding corporate loans–which is roughly the same level as in 2013, and a big increase from the 32% in 2016 (again, this is the share of outstanding loans; the chart above is the share of new loans made each year). This suggests that new loans to private firms rebounded in 2017-18 (probably more in 2017) as the economy recovered.

Second, on the industrial data. The fact that industrial SOEs are increasing their value-added faster than private companies is certainly notable. But SOEs and private companies tend to operate in different industries, so it can be hard to tease out the difference between sector effects and ownership effects. Industrial SOEs are concentrated in upstream, commodity-producing sectors, while private firms are more in downstream manufacturing sectors. It seems quite likely to me that the big decline in SOE value-added in 2015-16, and its rebound in 2017-18, have the same source: swings in commodity prices that had big effects on their profitability (value-added is basically profits plus labor compensation). The chart below uses monthly rather than year-to-date data, and we can see that the growth in SOE value-added has recently fallen back below that of private firms as steel and oil prices have come down.

Lardy is right that the fact that in these charts the red line (SOEs) is above the blue line (private firms) is significant and concerning. But if this year or next the blue line moves back above the red line, will that mean China’s private sector is out of the woods, and all is fine? I suspect not.